How to accept cryptocurrency payments as a business (2026 Guide)

Introduction

With over 700 million people worldwide now owning cryptocurrency (source: Crypto.com), businesses that ignore crypto could miss a rapidly expanding customer base.

The good news is, you no longer need deep technical knowledge to accept cryptocurrency payments, nor does your business need to hold crypto assets directly. Most companies now use crypto payment gateways, which allow them to accept digital currencies from customers while settling instantly in fiat to avoid volatility and accounting complexity.

In this guide, we’ll explain how to accept cryptocurrency payments as a business, outline the benefits and risks, and walk you through the practical steps involved in getting started.

How to accept cryptocurrency payments as a business (9 steps)

To accept cryptocurrency payments, most businesses use a crypto payment gateway, a third-party provider that processes digital-asset transactions much like a card processor handles traditional payments.

These gateways simplify compliance and technical setup by converting crypto into fiat automatically, so your business receives settled funds in your bank account (or virtual account) without holding volatile assets.

Here’s how it works.

Step 1 - Select your provider

You'll want to make sure you select a provider with the right technology, global network and compliance and risk controls to deliver effectively on your needs. Take a look at this practical checklist, for key evaluation criteria and questions to ask potential crypto processing providers, covering:

- Fees and rates

- Processing and settlement times

- Operational redundancy

- Compliance and risk

- Additional features like reporting, integrations and IBAN accounts

Once you've selected your provider, you'll need to go through onboarding and verification to set up your business account which can take a few weeks.

Step 2 - Integrate the gateway into your website

To add cryptocurrency payments to your checkout or deposit page, you'll need to integrate your chosen payment gateway provider.

Depending on your setup and provider, you can do this through plugins, hosted payment pages, APIs or other software tools provided by the gateway service. It can take anywhere from 2-8 weeks depending on your setup and internal resources.

For in-store payments, retailers will also usually require a physical device (similar to a card reader), which integrates with their POS system.

Step 3 - Optimize payment page for conversion

If you're using a hosted payment page it should be optimized for conversion, ensuring that the most popular or highest converting cryptocurrencies are prominently featured and the payment experience is easy.

If you're building a custom payment journey, your provider should be able to advise you on how to optimize them for the best experience and conversion rates.

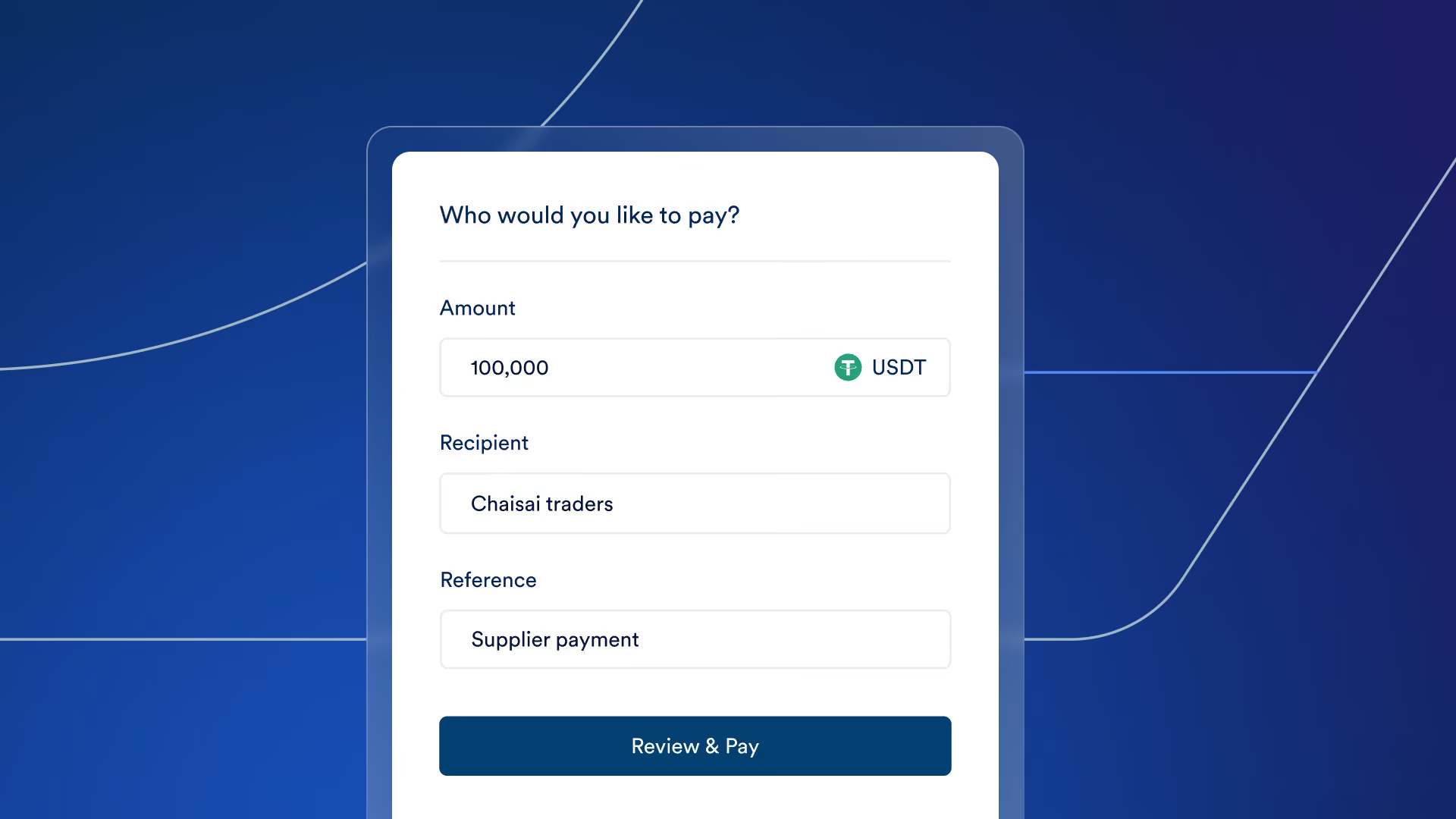

Step 4 - Customer selects crypto payment

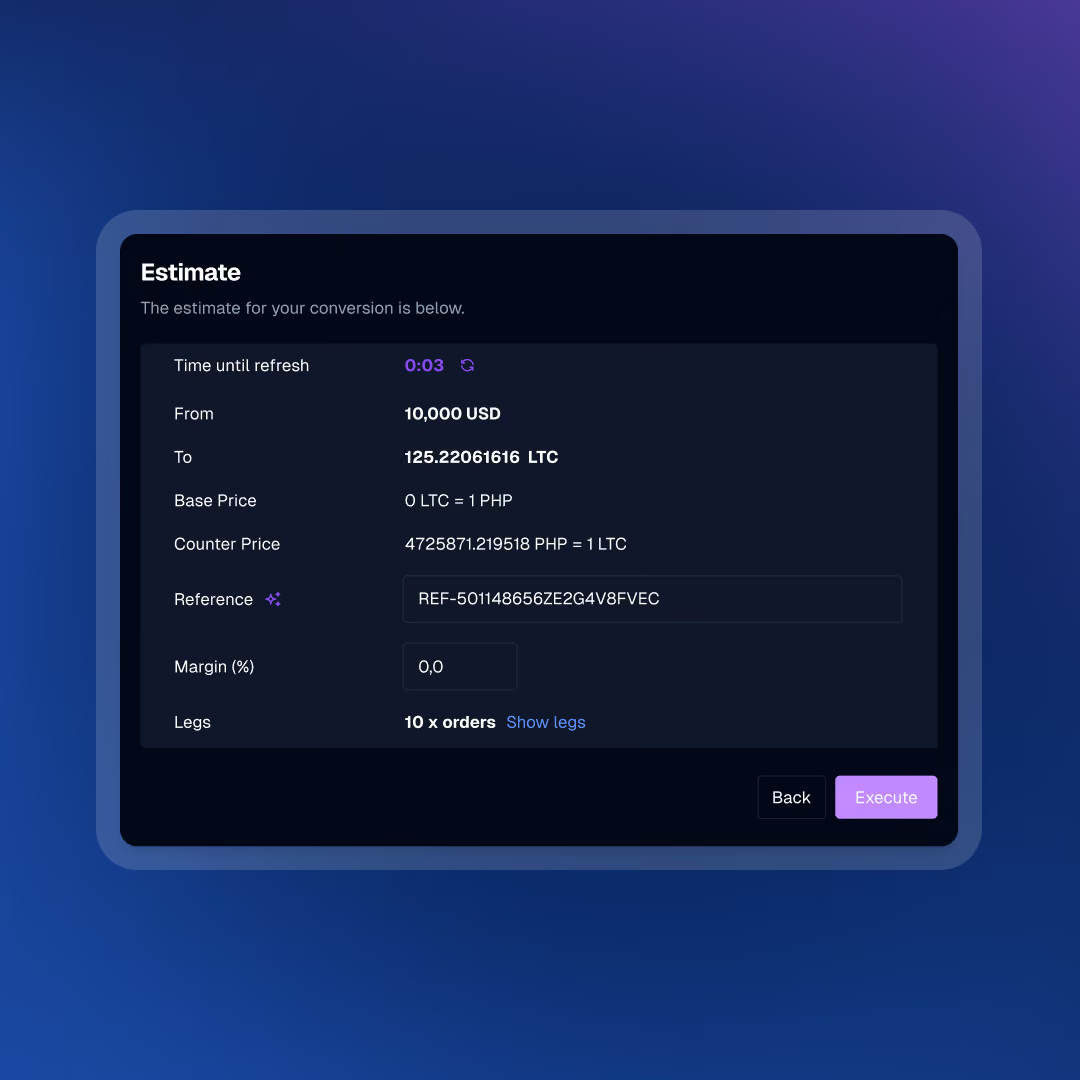

Once your new crypto payment experience is live, your customers can select to pay with cryptocurrency at your checkout from the list of available payment options. They choose which cryptocurrency they want to pay with, and they're shown the exchange rate by your provider.

They accept the exchange rate price, triggering an API request to your crypto payment processor who returns a payment link, restating the value of the payment and the cryptocurrency that the customer has requested to pay in.

Step 5 - Customer confirms payment details

The payment link will show the customer the amount of cryptocurrency they need to send, and the wallet to send it to (often represented by a QR code).

Step 6 - Customer connects their crypto wallet

To make the payment, your customer needs to open their own cryptocurrency wallet. Your payment provider should have integrations with popular crypto wallets making this step of the journey easier. Once they've connected their wallet, the customer confirms the payment and sends funds to the merchant's public address.

In practice, the payee wallet may be owned by the crypto payment processor, removing the need for you to hold any crypto assets on your balance sheet. If you don't want your customer to pay the processing fees, ensure that your provider takes its fees directly from you.

Step 7 - Payment is processed via the blockchain

When the payment is initiated, your payment provider submits it to the blockchain and it's checked by nodes to ensure the customer has enough funds to make the payment. Once verified, the transaction is submitted to a block, awaiting miners to validate it.

A transaction is typically approved after a validated block has been certified by 12 nodes, taking up to five minutes. The transaction is then completed and recorded on the blockchain. Some providers offer to guarantee settlement at this point so that you receive instant confirmation.

Step 8 - Successful payment is confirmed

Once the transaction is confirmed on the blockchain network, the crypto payment processing provider notifies both the customer and the merchant about the successful payment.

Step 9 - Settlement

If the retailer has chosen to receive payment in a cryptocurrency, the payment gateway provider will forward the funds to their wallet directly, minus fees. For fiat settlements, the crypto payment processor will convert the cryptocurrency and send the fiat funds to the merchant’s bank account, minus their fees. Some payment gateways offer instant conversion, while others provide daily or periodic settlements.

You now know how to accept cryptocurrency payments securely and settle them in fiat.

Let’s now look at what you else should keep in mind as you operate and scale your business’s crypto payment system.

Benefits and risks of accepting crypto payments

The benefits

Meeting customer demand

As noted in the introduction, more people want to pay with cryptocurrency, especially in emerging countries where financial exclusion rates are high. Businesses that offer popular cryptocurrencies at checkout are likely to be more competitive in these markets.

Fast, always-on settlement

Many national banking networks allow fast payments within a country, but that isn’t the case when you sell cross-border.

Most cross-border payments rely on the international SWIFT network and can take several days to settle depending on the region, especially when moving funds in and out of emerging markets. Your finance team may need to pre-fund accounts or deal with cash flow pressure.

When you settle on blockchains using digital currencies like stablecoins, payments can be nearly instantaneous and processed 24/7 (you’ll need to add time if you convert crypto to fiat). This eliminates the cash flow gap between your sales and revenue.

High average transaction value

Crypto holders tend to be higher income, higher spending, and complete checkout at higher rates BVNK customers for example in industries like FX trading report that average deposit values for cryptocurrencies can be 5-10x higher in some markets than payments made with credit or debit cards.

Predictability

Blockchain settlements are final. Customers can’t request chargebacks, which eliminates friendly fraud and related administrative costs. The predictability of crypto transactions also makes financial reporting and planning easier, giving you greater confidence in your numbers.

Reliability

Leading cryptocurrencies have proven over many years that they’re a secure way to transact. The large daily volumes processed on major blockchains demonstrate that they’re a reliable medium of exchange.

Adoption ease

As noted earlier, you can adopt crypto payments easily. You can outsource your entire crypto payment operation to a third party, giving your business all the benefits without taking on the risk or compliance obligations of holding crypto as an asset on your balance sheet.

Transparency

Although blockchains don’t directly reveal payer or payee identities, they make every transaction traceable through public addresses and immutable records. This visibility provides a high level of payment transparency, supports reconciliation and financial recordkeeping, and helps you track fund provenance and detect illicit activity.

The risks and considerations

While crypto and stablecoin payments offer many compelling advantages, you should also understand the operational and market risks involved. For a full summary of crypto assets risks see here.

Payer experience

The cryptocurrency payment experience is still developing. Many merchants see strong conversion rates for crypto payments, especially in countries where customers lack access to international credit cards, but the checkout experience still falls short of one-click e-commerce standards.

Price volatility

If you hold digital assets on your balance sheet, price fluctuations can cause losses. For example, Bitcoin reached a high of about $126,000 in 2025 and fell to as low as around $74,400 earlier that year. Most businesses avoid this risk by working with payment partners who instantly convert crypto into fiat.

Stablecoins such as USDT and USDC provide an alternative by maintaining value relative to the U.S. dollar. They now support annual on-chain transfer volumes of around $36 trillion as of July 2025, surpassing the total transactions of major card networks like Mastercard and American Express.

Regulatory compliance

Policymakers are moving toward clearer frameworks for digital assets, but rules still differ by region. This uncertainty can slow down adoption or limit your operations.To solve it, you should partner with a payment provider that prioritizes compliance and risk management, as this ensures adherence to KYC and AML standards while protecting your business from legal exposure.

Interoperability

Different blockchains and tokens don’t always connect easily with each other or with traditional financial systems. Some fintechs operate proprietary networks like Ripple/XRP, while others, including BVNK, integrate multiple blockchains and currencies. BVNK addresses this challenge through an API layer that moves funds seamlessly between networks.

Crypto payments for business explained

Understanding how crypto payments work helps you choose the right partners, manage risk, and spot new opportunities for your business. Here’s a quick primer.

If you’d like to learn more about use cases and payment flows. see our guide to building your stablecoin and crypto payment strategy.

Blockchain

A blockchain is a shared digital ledger that records every transaction across a network of computers. It operates independently of banks and card networks, so transactions can happen anywhere in the world, at any time. Because users can send value directly to each other, you avoid third-party delays and reduce settlement costs.

Cryptocurrency

Cryptocurrencies are digital assets exchanged across blockchains. They can act as both investment vehicles and payment instruments. Bitcoin (BTC) remains the largest, with a market cap above $2.3 trillion in 2025, representing nearly half of all crypto value.

A growing category of cryptocurrencies called stablecoins, such as Tether (USDT) and USD Coin (USDC), aim to maintain stable value by pegging their price to the U.S. dollar or other assets. Stablecoins now dominate crypto payments because they combine blockchain speed with fiat-like price stability.

Nodes and miners

Most blockchains operate in a decentralized way, meaning no single organization controls them. Instead, users collectively maintain the network. Coin holders typically take on two main roles: nodes and miners.

Nodes (that is, computers) witness and verify transactions while storing complete copies of the cryptocurrency ledger. If someone attempts to double-spend by sending two payments at the same time, the network’s nodes reach a majority consensus on which transaction occurred first. The network confirms that transaction on the blockchain and rejects the duplicate.

Miners dedicate a certain amount of computing power (known as ‘hash power’) to verify new blocks of transactions. In return, they earn newly minted coins and a transaction processing fee.

Wallets

A wallet stores the digital credentials that let you send and receive crypto payments. It can be custodial, where a third party (like an exchange or payment gateway) manages the private keys on your behalf, or non-custodial, where you hold full control of your funds. For business use, most companies rely on custodial wallets managed by their payment provider to simplify access, compliance, and recovery.

Cryptocurrency payment gateway

A cryptocurrency payment gateway (also known as a crypto payment processor) lets you accept digital payments from customers and receive settlement in fiat instantly. The gateway manages all the technical details: enabling blockchain transactions, maintaining compliance, managing wallets, and converting crypto to fiat. This setup lets you offer crypto payments to your customers without taking on volatility or regulatory complexity.

Get started with crypto payments for your business

Accepting crypto payments gives your business faster settlement times, lower processing costs, and access to new customer segments worldwide.

These advantages strengthen your cash flow and make it easier to compete in markets where card and bank payments are limited or expensive.

The simplest way to get started is to partner with a trusted crypto payment gateway that manages setup, checkout integration, fiat settlement, and compliance on your behalf.

At BVNK, we process billions in digital transactions each year for merchants worldwide. Our global payments platform makes it easy to accept and send crypto and stablecoin payments while settling instantly in fiat, without changing your treasury operations.

Learn more about crypto payments and how BVNK can support.

FAQs

How many businesses accept crypto?

According to recent data from Coinranking, approximately 36,000 businesses worldwide now accept Bitcoin payments in 2025, including global brands such as Subway, Starbucks, BMW, and Microsoft. The number of cryptocurrency owners has grown to an estimated 708 million people globally in the first half of 2025, according to Crypto.com’s Global Crypto Market Sizing Report.

What are the risks of accepting cryptocurrency?

The main risks of accepting crypto payments include price volatility if you hold digital assets on your balance sheet and the challenge of navigating a fast-changing regulatory environment. Stablecoins are becoming a popular alternative because they offer greater price stability. Many merchants minimize risk by working with payment partners who collect crypto on their behalf and settle funds in fiat. Experienced crypto payment providers can also handle much of the regulatory compliance work for you.

Can small businesses accept crypto?

Yes. Any small business with an internet connection and a crypto wallet can accept digital payments. In practice, most businesses use a crypto payment gateway provider to manage the checkout process, blockchain transaction processing, wallet management, and fiat conversion.

Can my business have a crypto wallet?

Yes. Any business can create one or more crypto wallets for different currencies. A custodial wallet is managed by a third party such as a crypto payment processor or exchange. The provider holds the private key and ultimately owns the crypto. A non-custodial wallet gives you control of the private key, so you own the coins directly. However, if you lose your private key, you lose access to your crypto permanently. When choosing a wallet, consider how easily it integrates with your checkout system. Many businesses simplify this by outsourcing wallet management to their crypto gateway provider.

Why is it difficult for most businesses to accept bitcoin as a form of payment?

It’s not technically difficult to accept bitcoin, but some businesses hesitate because of price volatility and regulatory uncertainty. Volatile prices make it harder to price products consistently, and regulations differ widely by region. Most businesses that accept crypto avoid these issues by working with a payments partner who collects and converts bitcoin on their behalf, settling directly in fiat currency.

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

Never miss an insight.