Build your stablecoin strategy

.avif)

1. Executive summary

The financial world is undergoing a shift as seismic as the transition from analog to digital communications. At the heart of this shift are stablecoins. Stablecoins are creating a new base layer for financial services — one that’s global, real-time and accessible 24/7/365.

As stablecoin adoption grows, so does their utility. In just six years, stablecoin supply has surged from near zero to $250 billion, with forecasts of $2 trillion by 2028. Real-world stablecoin payments meanwhile have grown from half a trillion in 2020 to $7.4 trillion in the last 12 months (source: Visa).

Recent developments, such as Circle's IPO and the launch of stablecoins by major financial institutions like JPMorgan and Fiserv, underscore this momentum. At BVNK, we believe we're moving toward a world where a large majority of global money will exist in the form of stablecoins. In the next 10 years, stablecoins could reach 20% of the global cross-border payments market (from c.3% today).

This guide aims to help you capture your share of this opportunity. It bridges the gap between stablecoin ambition and implementation with:

- Use case selection:Implementation models with personalized API and UX demos, fund flows and case studies.

- Business case support:Market data and metrics to build your internal business case.

- Risk mitigation:Regulatory overviews and compliance approaches compared.

- Pricing intelligence:Provider fees and cost levers demystified.

- Delivery roadmap:From portal to API to embedded, deployment options explained.

Every fintech and global enterprise needs a stablecoin strategy. We’re here to help you define yours.

2. Choose your use case

At BVNK, we support businesses and fintechs to send, receive, store and convert stablecoins. The most common use cases we serve are:

- Send:pay suppliers, partners, workers and customers globally in stablecoins, from a fiat balance. Or use a combination of stablecoins and fiat payment rails to accelerate cross-border payments to businesses and individuals.

- Receive:accept stablecoin payments from customers or partners, auto-convert to fiat.

- Store:hold funds in stablecoin-linked accounts with access to ACH, Fedwire, SEPA, Swift and all the major blockchains.

- Convert:move between currencies and on/off-ramp in one platform.

We serve these use cases via two delivery models:

- Managed payments:for businesses that want to enable stablecoin payments fast, without handling crypto. They leverage BVNK’s custody, liquidity and licensing via our Portal, API or Embedded offering.

- Self-managed payments:our Layer1 infrastructure-as-a-service for those seeking scale and control. Connect your own licences, custodian and liquidity partners – or use BVNK’s services where it fits.

To learn more about delivery models, go to: Select your delivery model

Read on to learn about popular use cases, see what market leaders are building and test drive solutions with our personalized API demos for Send payments, Receive payments and Launch stablecoin wallets.

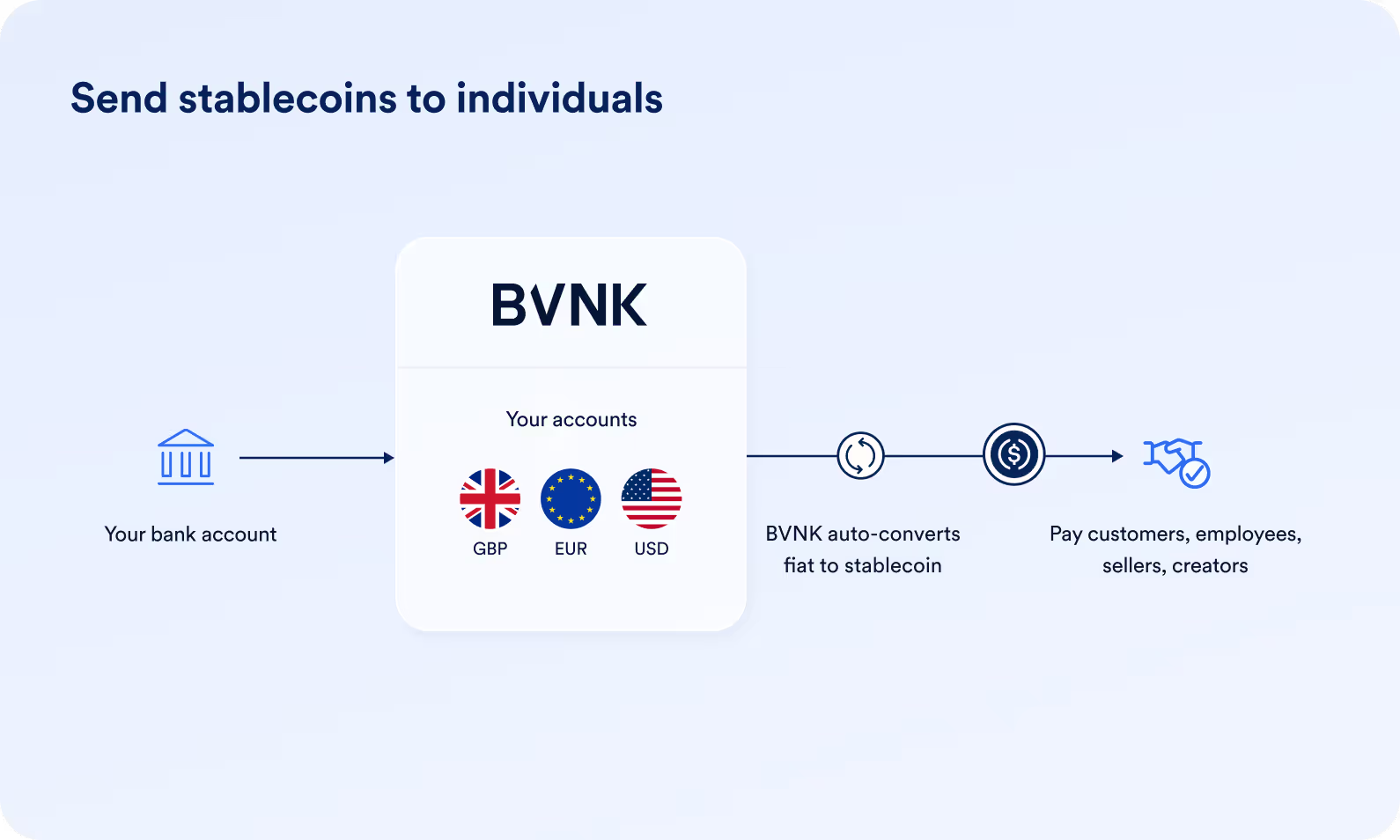

Send stablecoins to businesses or individuals

In a nutshell:

Make payments to business partners, suppliers and merchants in stablecoins globally, or let workers, customers, sellers, creators and hosts get paid in stablecoins – from a fiat balance.

Most used by:

Payment Service Providers, Marketplaces, Trading, Gaming, Employer of Record, Payroll, Social and Tech platforms.

Adoption drivers:

- Settlement delays using traditional correspondent banking system.

- Demand to receive payment in stablecoins.

- Problems getting local banking access.

- Unpredictable or high FX fees via traditional correspondent banking system.

Why are businesses integrating stablecoin payouts?

How it works:

- Store funds in USD, EUR or GBP in named accounts on the BVNK platform (deposit via Swift, ACH, Fedwire, SEPA, Faster Payments).

- Request stablecoin payout via API or the BVNK portal.

- BVNK automatically converts to stablecoins on your behalf on payout (no need to hold crypto).

- Access full transaction reporting via the BVNK platform.

Example: Your customer withdraws in stablecoins.

- Add stablecoin withdrawal option in your platform, which sends API request to BVNK.

- Your user specifies the amount they want to withdraw and adds their wallet address. They’re shown the payment details including exchange rate and any fees. You can also set payout conditions via API (eg when a product is sold, when a guest’s stay is over) and trigger the payout yourself.

- BVNK automatically converts on payout (no need to hold crypto), updating your fiat wallet balance.

The flow of funds for a stablecoin payout to an individual.

Deel teams up with BVNK to pioneer instant payments for workers worldwide

Challenge:

The global freelance workforce is thriving, growing 15x faster than traditional jobs, while the global gig economy market is expected to triple in size by 2032. And with the rise of global HR services and employer of record platforms like Deel – it’s easier than ever for businesses to hire and manage freelance talent globally.

Despite this, paying workers overseas remains a challenge. Today’s clunky cross-border payment systems can leave workers waiting days for money – only to lose out to unfavourable currency conversions at the last mile. Employers meanwhile are held back by tied-up capital and exposed to foreign exchange risk.

Solution:

In Spring 2024, Deel teamed up with BVNK to enable stablecoin payouts to global contractors. With BVNK's infrastructure, workers employed via Deel can fast-track wage payments with dollar-backed stablecoins like USDC, receiving them in minutes not days.

With BVNK's auto-conversion capabilities, there's no need for the Deel team to handle crypto. They simply fund their BVNK account in USD, EUR or GBP, and funds are converted automatically on payout. With this solution in place, Deel can ensure a seamless service for contractors, while remaining at the forefront of global payments innovation.

Result:

- Settlement time reduced from 3-5 days to near instant

- Strong adoption from contractors in Latin America and in markets with local currency fluctuations, with 125,000 successful payouts processed

- 10,000+ contractors in 100+ countries have opted to paid in stablecoins

1/3

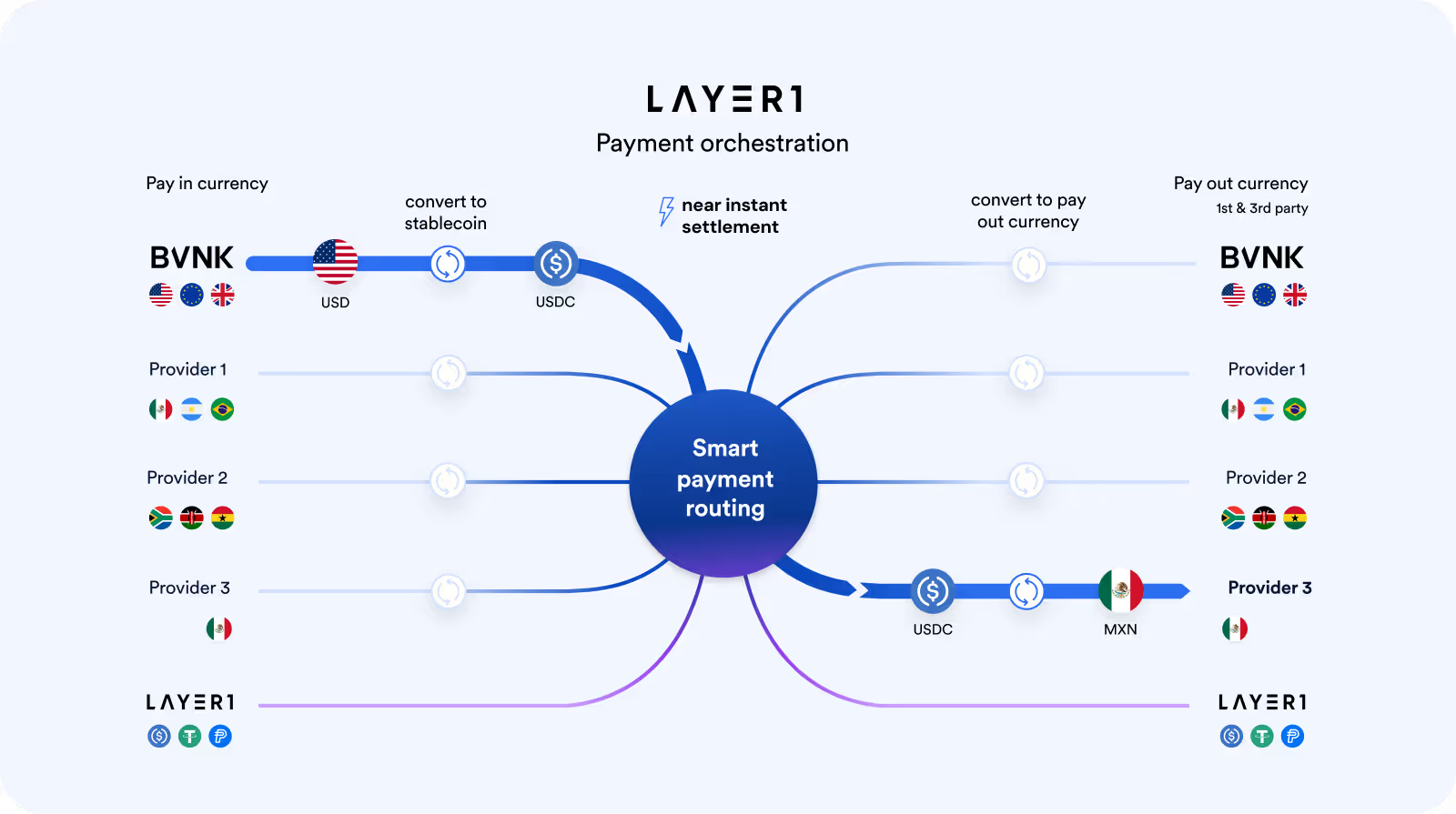

Send cross-border payments via stablecoins

In a nutshell:

Mixing stablecoin and local fiat payment rails to accelerate cross-border payments to businesses and individuals. For example to settle suppliers globally or facilitate remittance payments. Sometimes called 'the stablecoin sandwich'.

Most used by:

Remittance companies, Fintechs, PSPs, Trading platforms, Gaming platforms

Adoption drivers:

- Reducing settlement delays vs using only fiat payment rails.

- Avoiding high FX fees converting using traditional banking rails.

- Avoiding costly prefunding of accounts around the world (required to enable ’instant’ payments in the absence of instant cross-border settlement).

-

How it works:

- Layer1 (BVNK’s infrastructure-only product) orchestrates currency conversions and international transfers, making it simple to send money across borders.

- Layer1 provides the tech and smart routing.

- You manage the relationships with on-ramp, off-ramp and fiat payout providers.

- BVNK acts as a liquidity provider integrated with Layer1 for USD, EUR, GBP.

Example:

- Deposit:add USD to your BVNK account via Layer1.

- Request:send payout instruction via Layer1 for recipient in Mexico.

- Behind the scenes:Layer1 converts USD to stablecoins, then auto-routes via your local partners in Mexico

- Delivery:recipient receives Mexican pesos directly in their local bank account.

Layer1 from BVNK orchestrates currency conversions and international transfers.

Demo: Send stablecoins

Create an instant personalized API & UX demo to see how stablecoin payouts could work in your platform.

.svg)

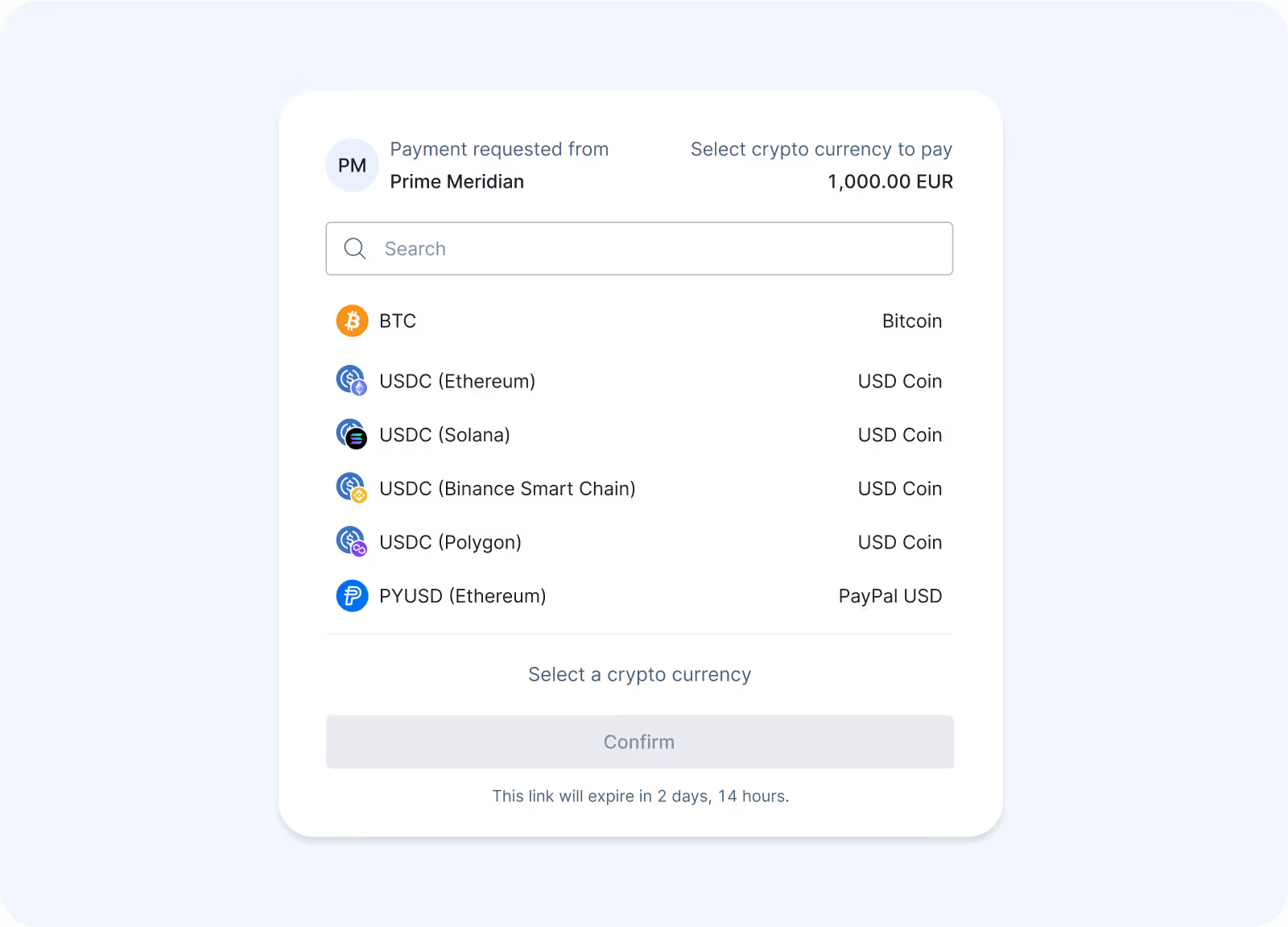

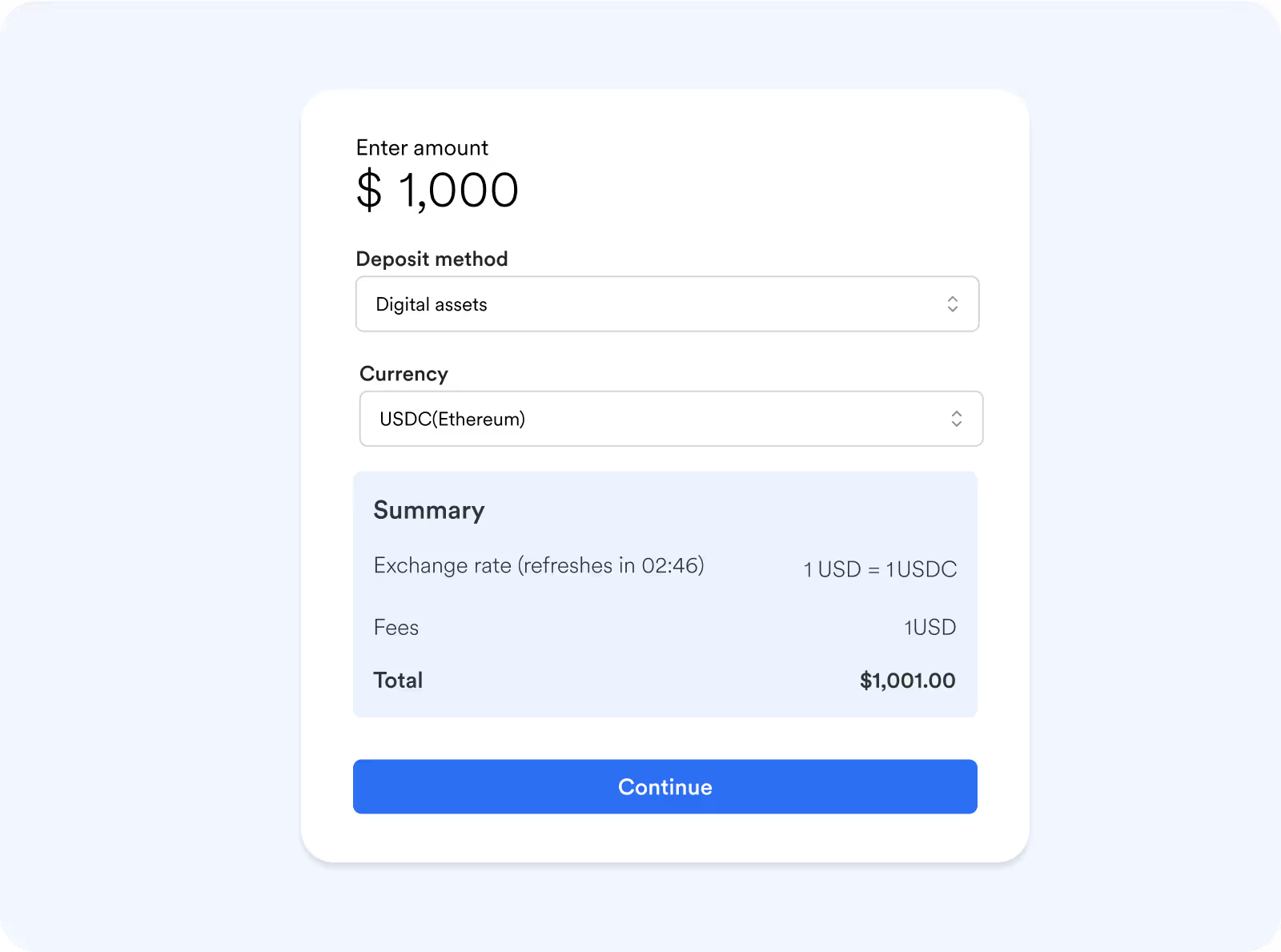

Receive stablecoins from customers

In a nutshell:

Add stablecoins as a customer payment option on your checkout or deposit page. Funds are automatically converted to your preferred fiat currency.

Most used by:

Luxury ecommerce, Travel, Marketplaces, Payment Service Providers, Gaming, Trading.

Adoption drivers:

- Demand from customers to pay in stablecoins.

- Customer problems with traditional payment options in emerging markets (eg cards not valid for international transactions or transactions blocked by card providers).

How it works:

- Integrate BVNK’s pre-built payment pages or build your own custom front end using our API.

- Your customer selects to pay/deposit in stablecoins and connects their crypto wallet to complete the payment. Option to give dedicated crypto addresses to VIP users for anytime payments. Payments made on the wrong chain are auto-routed to the right chain by BVNK.

- BVNK auto-converts to your preferred fiat currency (USD, EUR, GBP) and updates your balance on the platform.

- Withdraw to your own bank account or use to fund third party payouts with BVNK (eg via Swift, ACH, Fedwire, Faster Payments, SEPA).

The flow of funds for a stablecoin pay in.

Trade Nation unlocks new business and increases deposits by 260%

Challenge:

Trade Nation's customers in Asia struggled to top up trading wallets using traditional payment methods. In some countries, cards weren't valid for international transactions or were blocked by card providers. Bank payments required manual processing, hindering time-sensitive trading.

Solution:

Trade Nation integrated BVNK's hosted payments page to enable customer deposits and withdrawals in 15 digital currencies.

Result:

- 260% increase in deposit volume after implementation

- 56% of deposit volumes in new markets now paid in cryptocurrencies

- Unlocked previously inaccessible customer segments in key markets

- Reduced operational overhead by eliminating manual payment processing

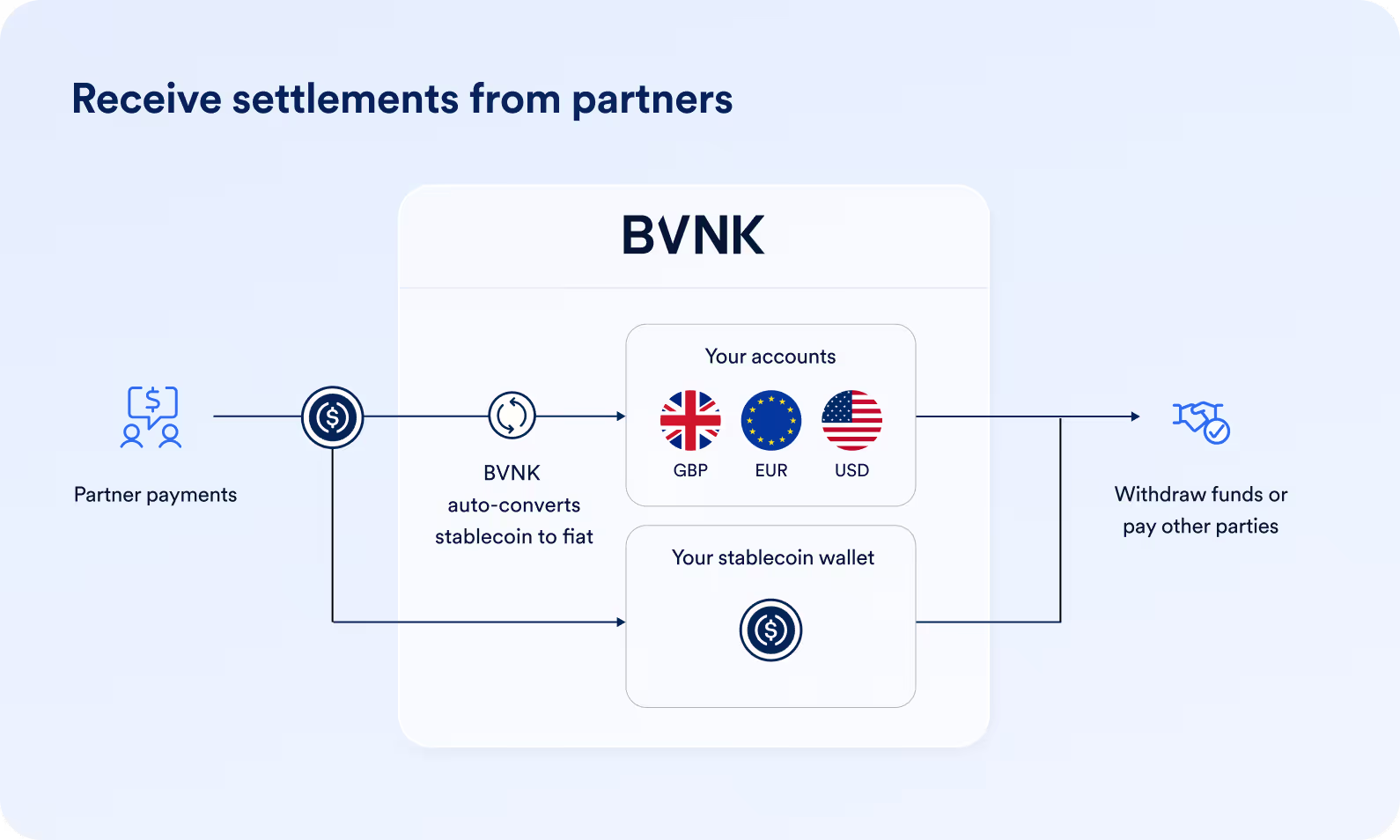

Receive settlements from partners

In a nutshell:

Receive settlements from affiliates, business partners or local payment partners in other countries – hold in stablecoin wallets or auto-convert to fiat currencies.

Most used by:

PSPs, Trading platforms, Gaming

Adoption drivers:

- Demand from partners to use stablecoins.

- Cross-border settlement delays using traditional correspondent banking system.

How it works:

- Create payment requests:generate payment links to share via email, SMS, or WhatsApp.

- Set up channels:give partners dedicated addresses for regular deposits.

- Receive funds:partners pay using their preferred cryptocurrency. Payments made on the wrong chain are auto-routed to the right chain by BVNK.

- Choose your destination:

- Option A: BVNK converts to your preferred currency and holds in your account.

- Option B: funds go directly to your stablecoin wallet.

- Use your funds:withdraw to your bank account or use for future BVNK payouts.

The flow of funds for receiving a stablecoin settlement from a business.

Demo: Receive stablecoins

Create an instant personalized API & UX demo, to see how stablecoin pay-ins could work in your platform.

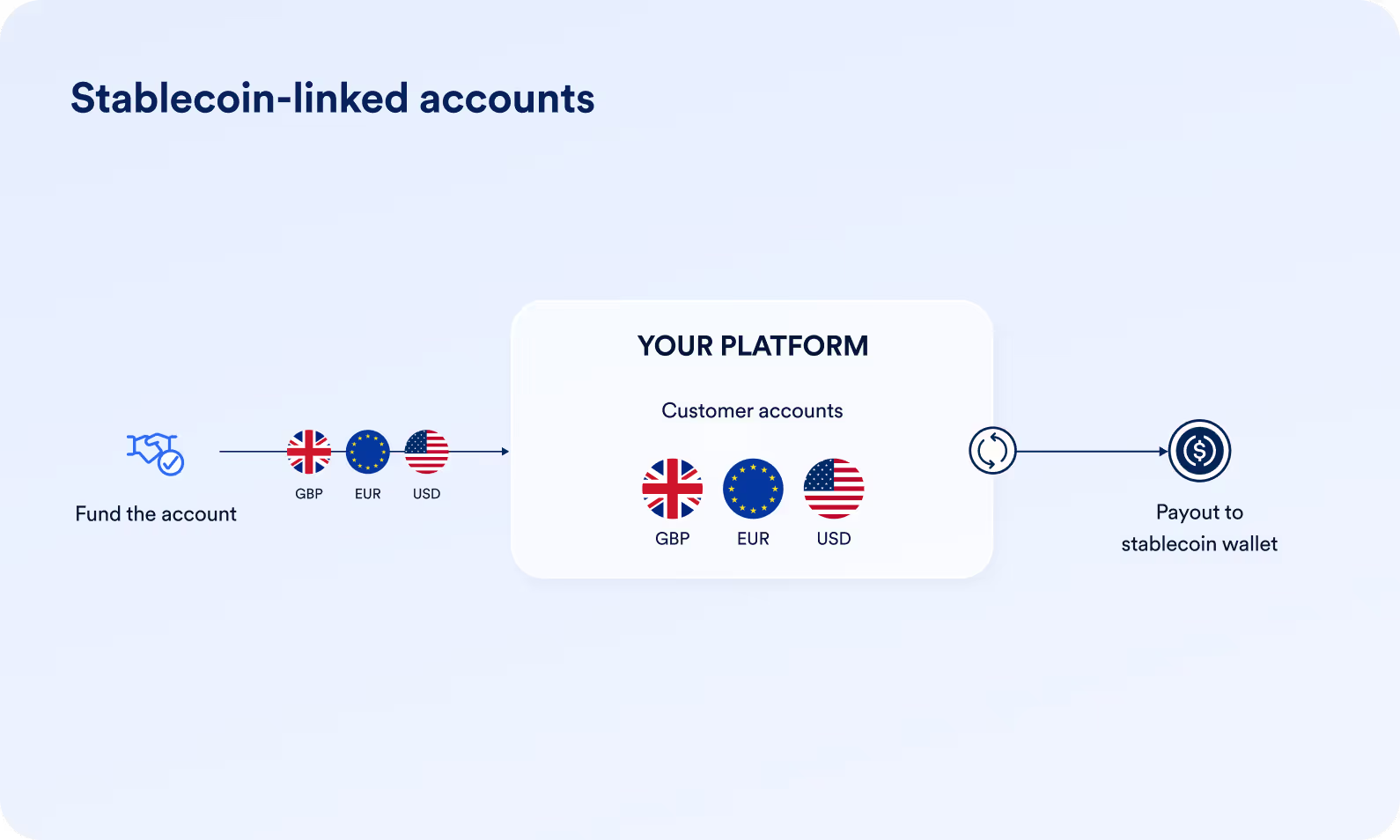

Launch stablecoin wallets

In a nutshell:

Let your customers send and receive stablecoin payments from USD, EUR or GBP wallets, with access to major payments schemes like Swift, ACH, Fedwire and SEPA.

Most used by:

PSPs, Fintechs, Payroll, Employer of Record

Adoption drivers:

- Customer demand for stablecoin payments.

- Competitive pressure to innovate/differentiate.

How it works:

- Integrate:with BVNK’s API so your customers can manage payments in fiat and stablecoins in your ecosystem.

- Opting in:your customer accepts BVNK’s terms in your platform. In the background, you pass KYB/C data to BVNK via API. BVNK initiates verification and notifies your customer.

- Creating an account:once verified, your customer creates their first wallet in your platform.

- Making a deposit:you/your customer deposit funds via ACH or Swift, or via their crypto wallet.

- Creating a payout:once your customer's wallet is set up, they can start using it. Eg they could pay out USDC from a USD wallet. BVNK auto-converts in the background and executes the payment.

- Depositing stablecoins:your customer can also deposit stablecoins. They select the stablecoin option, copy the wallet address and go to their crypto app to complete payment. BVNK auto-converts and their USD balance is updated.

Example 1: Your customer wants to pay out to their suppliers in stablecoins.

- Fund:you or your customer fund a named wallet in USD/GBP/EUR in your platform (powered by BVNK).

- Initiate:customer selects to pay out in stablecoins in your platform.

- Send:BVNK automatically converts the fiat currency to stablecoins and sends to the supplier's wallet address.

Example 2: Your customer wants to on-ramp from USD to stablecoins in your platform, then off-ramp back to USD.

- Deposit:customer sends USD from their bank → funds appear in your platform as stablecoins.

- Hold:funds remain as stablecoins in customer's wallet on your platform.

- Withdraw:customer requests USD withdrawal → BVNK auto-converts stablecoins back to USD and sends to their bank.

The flow of funds for a customer payout using a stablecoin wallet

Worldpay enables stablecoin payouts for global businesses in collaboration with BVNK

Challenge:

Worldpay, one of the world's largest payment processors, faced growing demand from global business customers for instant stablecoin payouts.

Solution:

This collaboration will enable Worldpay’s clients to pay out to customers, contractors, creators, sellers, and other third party beneficiaries in stablecoins across 180+ markets nearly instantly, without having to hold or handle stablecoins themselves. Worldpay clients will be able to access this new stablecoin payout service through their existing integration with Worldpay’s payouts platform. Stablecoins will be the first type of digital asset enabled as a payout option on Worldpay’s payout platform, complementing the existing 135 fiat currencies currently available.

Result:

- Expanded payment capabilities across Worldpay's $2.3+ trillion commerce network

- Competitive differentiation in a crowded payment processing market

- Reduced payment friction for global merchants with cross-border needs

Demo: Stablecoin wallets

Create an instant personalized API & UX demo, to see how your customers can create accounts and make payments in stablecoins or fiat in your platform.

3. Make your business case

Key datapoints to help you build a business case for stablecoin payments, including global adoption data, settlement information and cost comparisons.

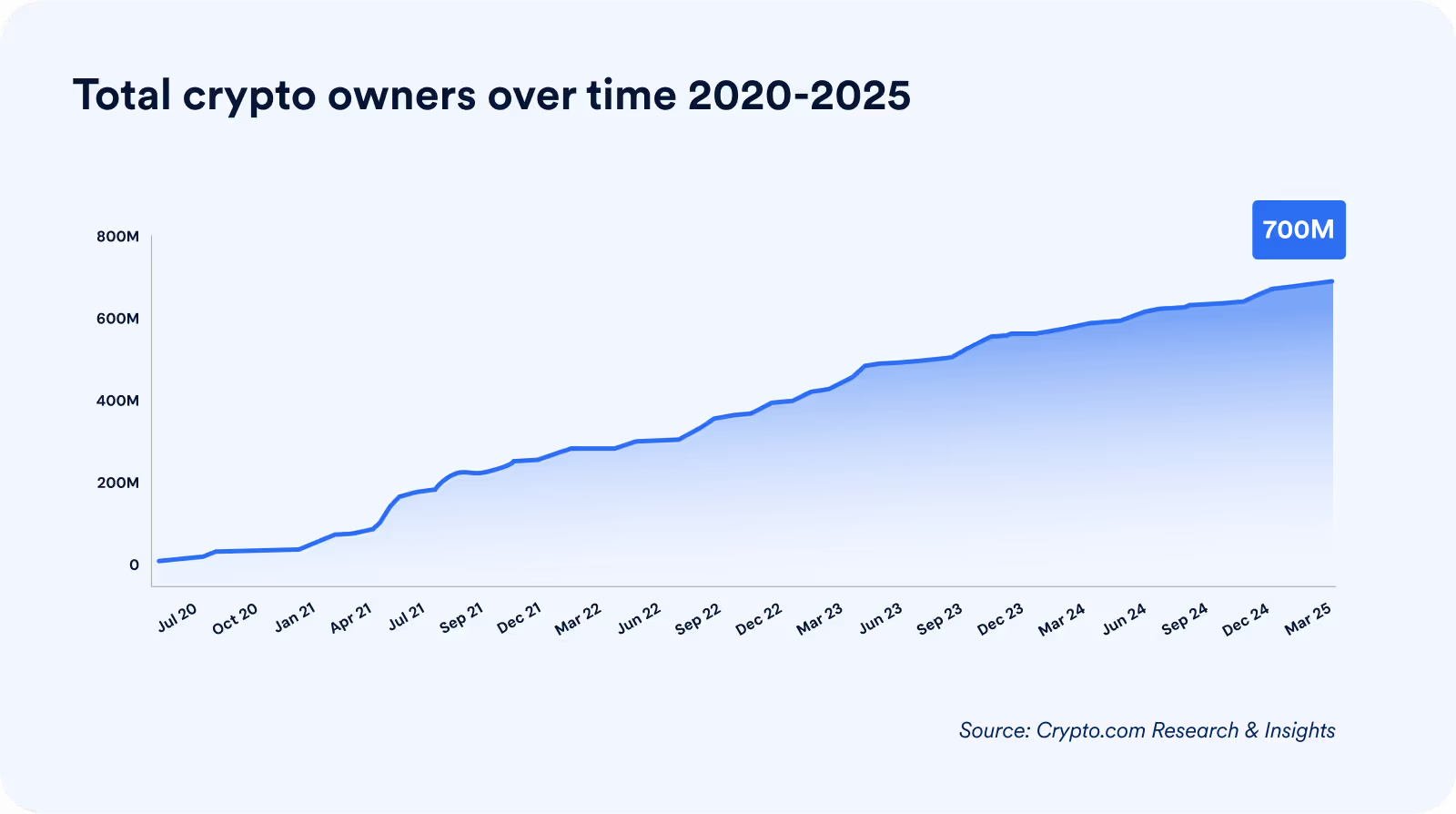

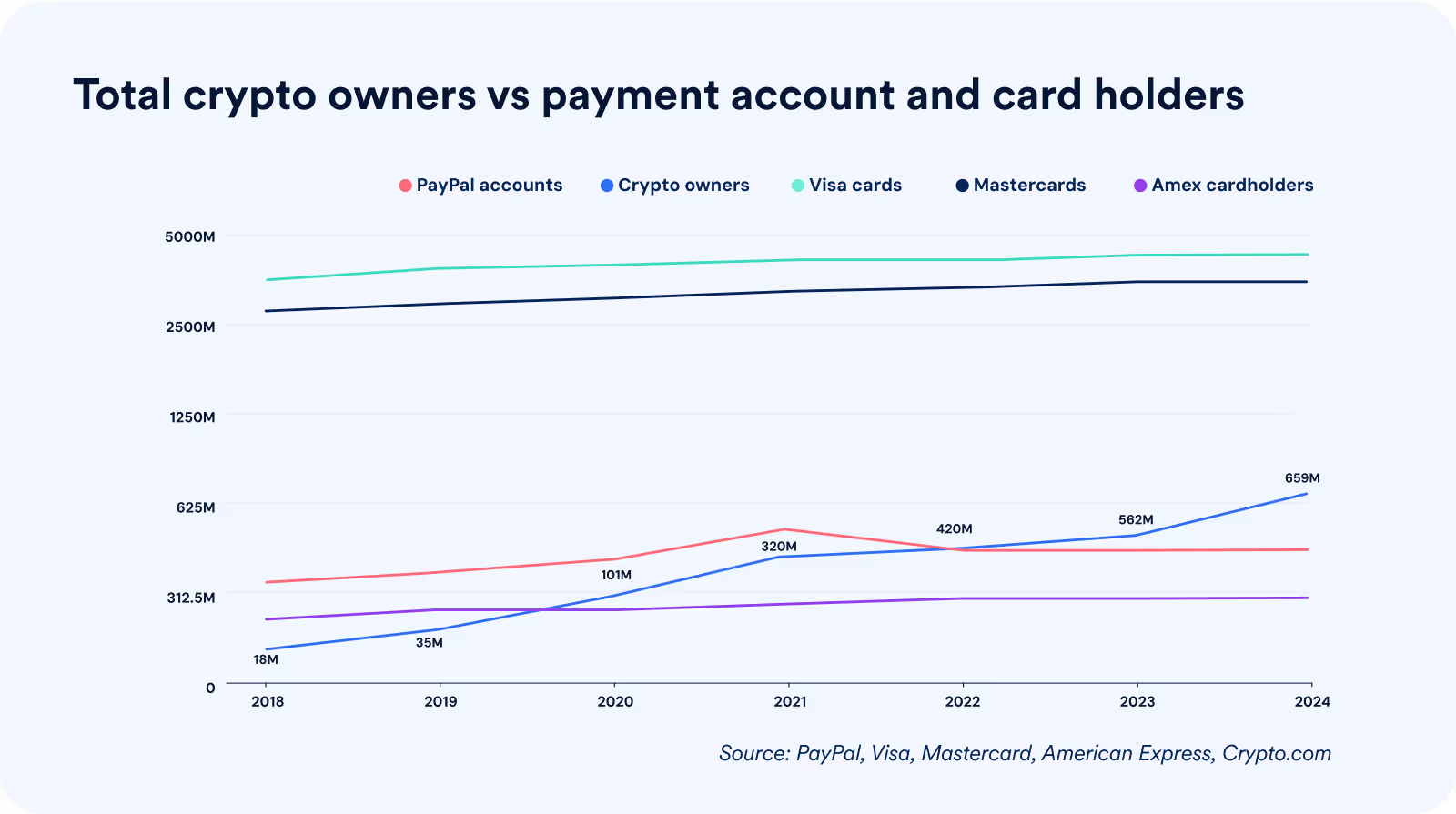

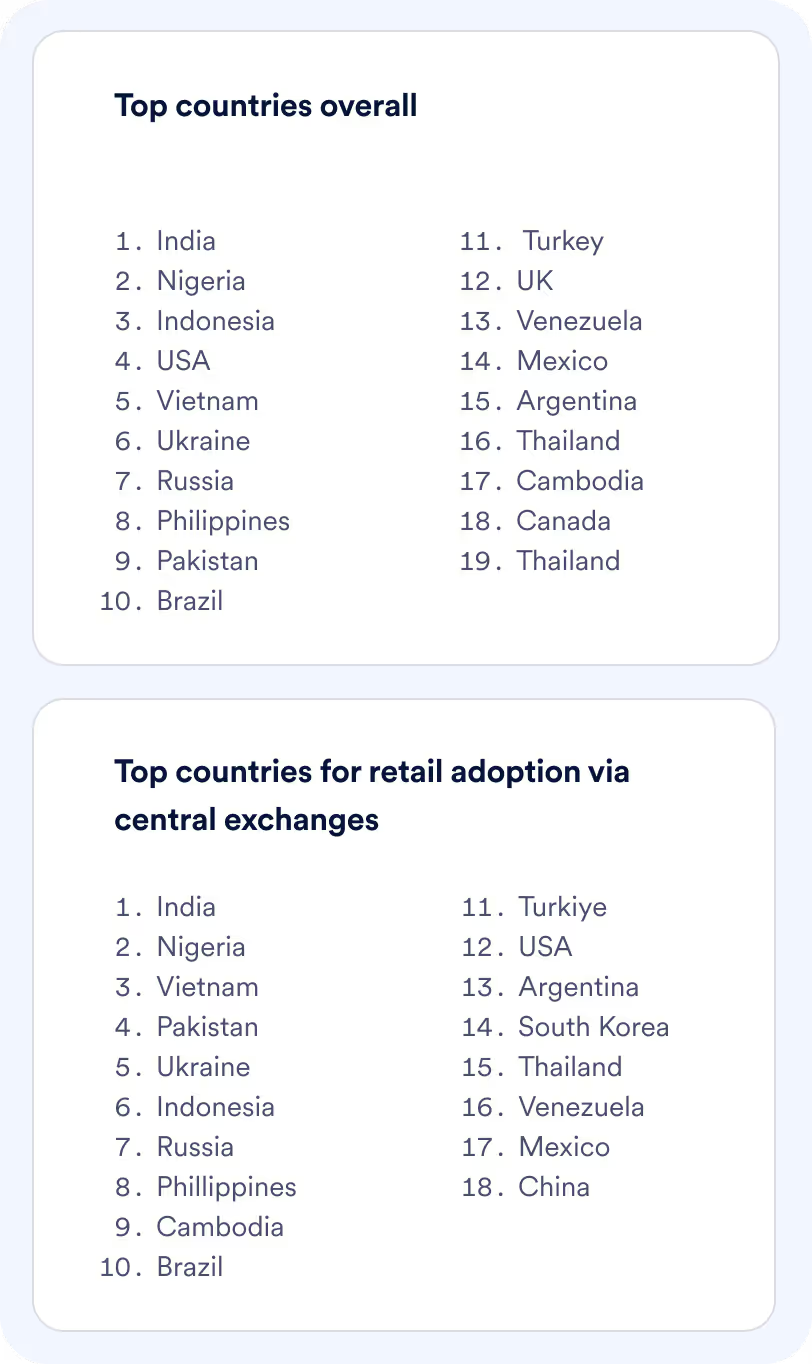

Crypto ownership

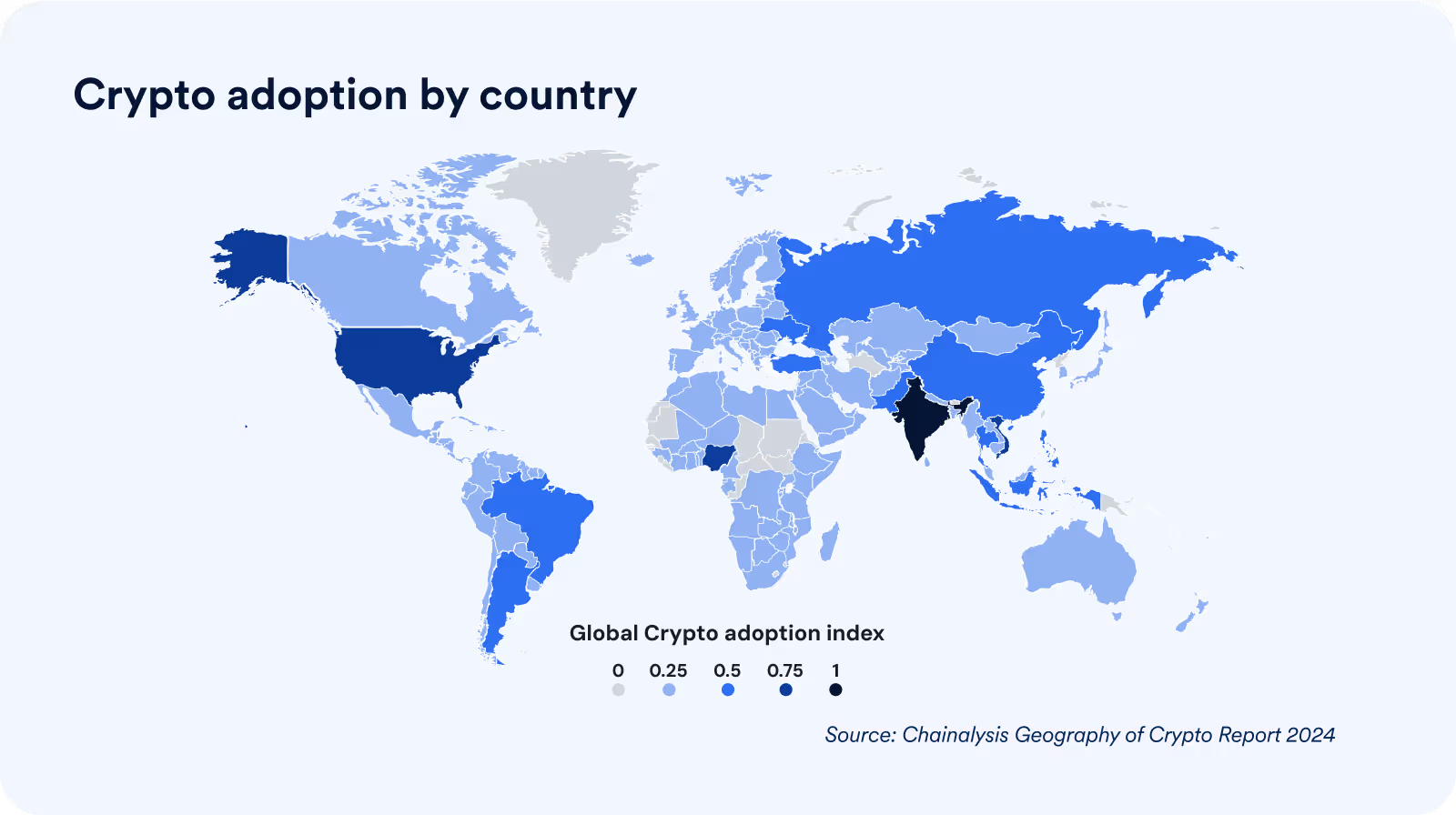

Crypto adoption by country

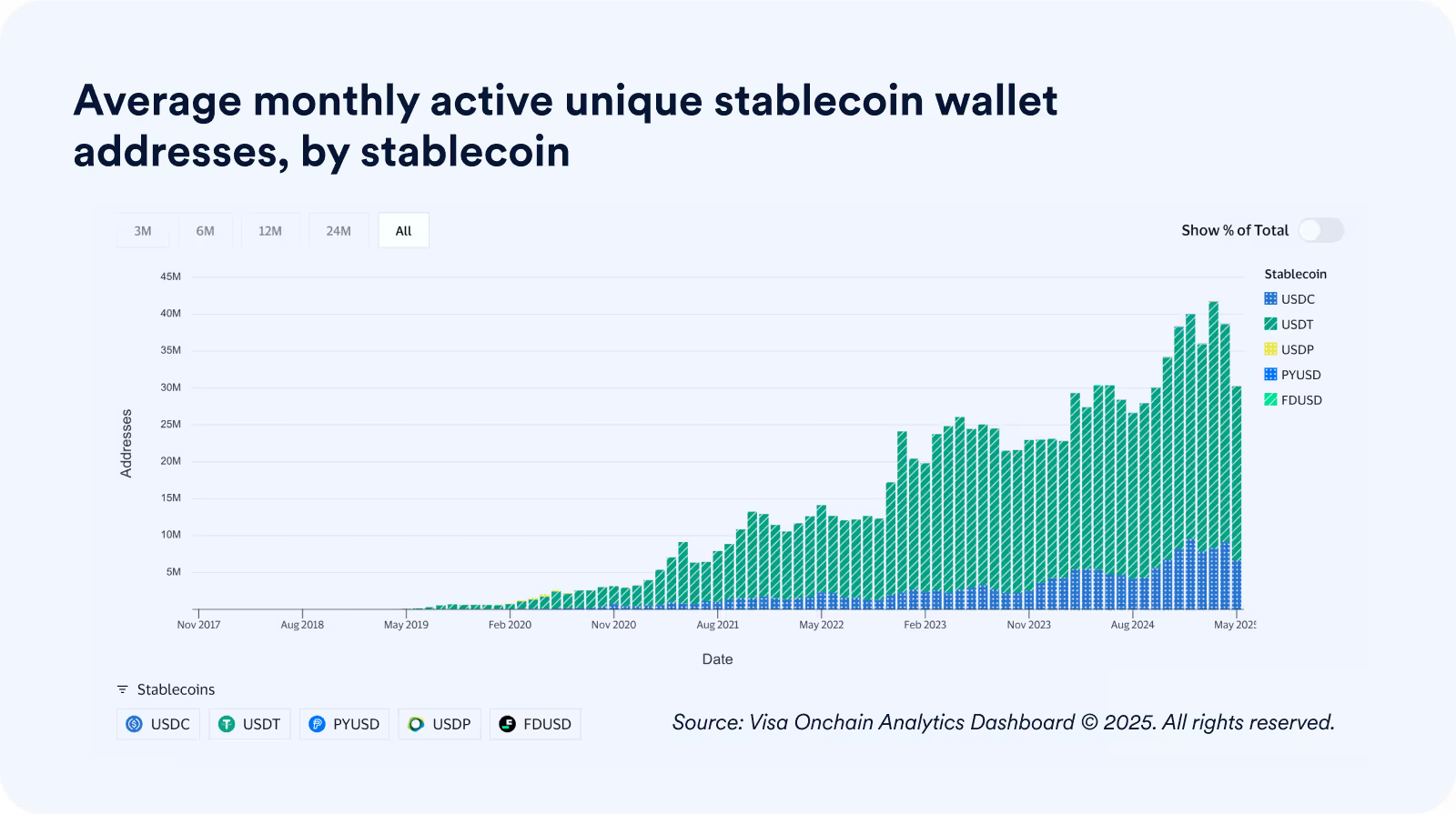

Stablecoin active wallet addresses

Monthly active unique stablecoin addresses peaked at their highest ever in May 2025, at 416.21 million, a 40% YoY increase.

For the latest active stablecoin wallet data, please see: Addresses | Visa Onchain Analytics Dashboard

Stablecoin transaction volumes

When looking at stablecoin volumes, it’s important to distinguish between transactions that facilitate crypto trading – and those estimated to be for real-world payments use cases.

Source: Visa Onchain Analytics 2025. For up to date stablecoin transaction volume, please see: Transactions | Visa Onchain Analytics Dashboard

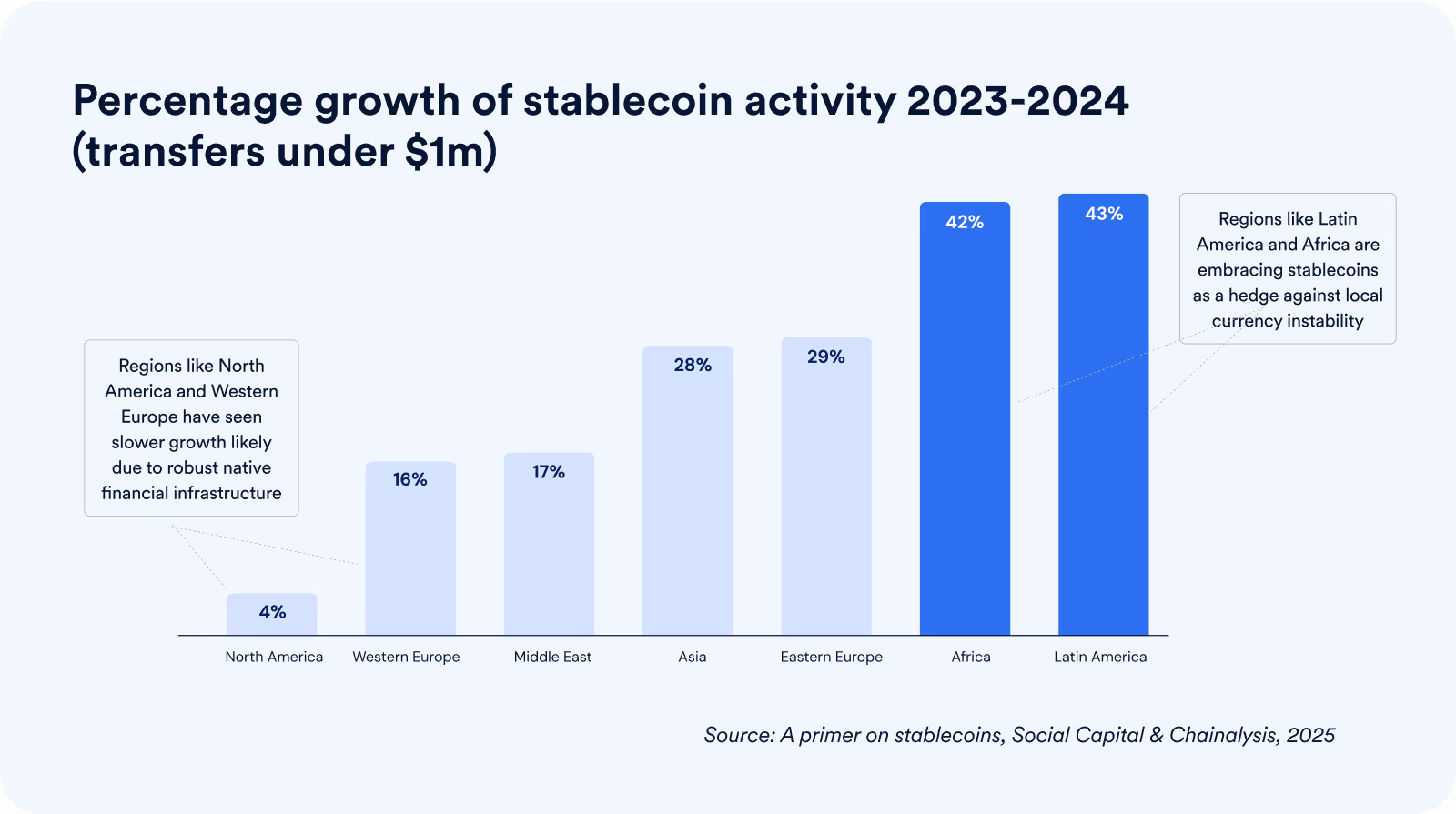

Growth in stablecoin activity by region

Source: A primer on stablecoins, Social Capital & Chainalysis 2025

Source: A primer on stablecoins, Social Capital & Chainalysis 2025

Settlement times

Blockchain settlement speed

How long it takes to settle a blockchain transaction depends on the blockchain, the cryptocurrency and network congestion. For example, some cryptocurrencies like Solana can have almost immediate transaction confirmations, while Bitcoin can take around 40 minutes. Most cryptocurrencies require a few confirmations (additional blocks in the blockchain) for transactions to be deemed validated and irreversible.

Below, you can find the average times on BVNK to settle stablecoin transactions vs correspondent banking (Swift) alternatives.

On and offramp time

Converting into and back from fiat currencies adds settlement time. Note that the speed of on and off ramp to fiat will differ based on provider, local market rails and available liquidity.

For example:

- If the destination market has real-time payment (RTP) rails available, settlement will usually be in minutes (eg MXN, BRL).

- If the destination market does not have RTP rails or the payout partner does not have access to these rails, it might be same day settlement or T+1 (eg COP, ZAR).

Transaction fees

Below is an indicative guide to show where significant savings can be made using stablecoins for cross-border payments. Note that fees vary according to provider, currency, liquidity and volume. See: Get smart on pricing

Payment capabilities comparison

*Note: won’t apply to on and offramp. Operating hours of stablecoin payment providers may differ

Note: stablecoin payment providers like BVNK allow you to configure custom limits for payments as needed.

4. Understand licensing and compliance

Get up to speed on general crypto regulatory developments by region and compare KYC/B compliance models.

Licensing and regulation overview

A number of comprehensive regulatory regimes have emerged for crypto over the last few years. While they differ in specifics, they all focus on a set of core principles: customer protection, market stability and market integrity.

Regulators look to achieve these outcomes in different ways:

- Licensing and/or registration to ensure crypto service providers are subject to AML obligations and beyond.

- Rules on how businesses can promote or market crypto to consumers.

- AML compliance rules to make sure that providers are carrying out customer due diligence, transaction monitoring and reporting.

Below we summarise crypto regulatory developments in the EU, UK, USA, Singapore, Hong Kong, Middle East and Latin America as of June 2025.

Travel Rule for Crypto in force.

HM Treasury published draft crypto legislation in 2025.

Travel Rule in force.

Travel Rule in force.

Stablecoins Bill passed, set to take effect in 2025.

Travel Rule in force.

Saudi Arabia developing a national regulatory framework in 2025.

Travel Rule varies: in force in crypto hubs.

Varies by country.

Mexico expected to adapt finech law to better address crypto.

Travel Rule implementation uneven but progressing.

Compliance models compared

Your stablecoin partner may offer different compliance options which impact your obligations (eg whether you need to carry out KYC/B), as well as the capabilities you can access. Here we compare models offered by BVNK.

stablecoin wallets and payments.

stablecoin wallets and payments.

marketplaces, employer of record, payroll, remittance, gaming, trading.

marketplaces, employer of record, payroll, remittance, trading.

5. Get smart on pricing

Understand typical provider fees and the cost levers affecting price.

Fees charged by a stablecoin provider

The following are typical examples of fees charged for stablecoin payments. Choose a payments partner that gives you flexibility on how you charge for stablecoin transactions (eg enabling you to choose whether or not to pass on certain fees to your users).

Note: to discuss custom pricing for your needs, please reach out to the BVNK team

Eg for a $5000 USDT transfer:

Ethereum (ERC-20): ~$1-5

Solana: ~$0.00025-0.001

TRON (TRC-20):~$1-3 Bitcoin: ~$1-20

OR users.

Some providers won't charge if the cost is very low. BVNK for example only charges for Ethereum, Bitcoin, and Tron.

Note: providers may not charge for deposits into their platform.

Higher spreads can decrease conversion on a pay-in, so find a provider that gives you flexibility on whether to apply this fee, or whether it's baked into your processing fees.

Factors affecting pricing

Sending money via blockchain is often cheaper than via bank transfer, but it can depend on a variety of factors.

Blockchain factors

- Network:Fees vary between blockchains, with some optimized for lower cost transactions. Blockchains also use different consensus mechanisms (eg proof of work, proof of stake), which impacts cost. Learn more

- Network demand: Blockchain network fees are dynamic: higher demand for processing can increase the price of network fees, as more users compete for limited block space.

- Transaction complexity: The complexity and size of transactions can also affect network fees. Eg smart contract interactions typically cost more than simple token transfers.

Market factors

- Your volume:The bigger your volumes, the better the pricing you can access from your provider.

- Your provider’s volume: Established providers who process higher volumes across their entire client base will have access to better pricing from banks, issuers and liquidity providers.

- Strength of your provider’s partnerships: Strong, direct partnerships with stablecoin issuers and liquidity providers will enable your provider to access cheaper prices to pass on to you.

- Liquidity: Liquidity of particular stablecoins affects exchange rates when converting in and out of fiat.

- Risk status: If your business operates in a higher risk industry, your provider might need to carry out enhanced due diligence, which may impact pricing.

6. Select your delivery model

From portal to API to embedded, compare deployment options with BVNK and resource implications.

Managed payments

Perfect for customers seeking an all-inclusive solution, with custody, compliance and liquidity managed under one roof.

(post compliance onboarding), 2-8 weeks for API integration.

Self-managed payments

Manage your own wallet keys, bring your own licensing and integrate your chosen liquidity partners. Ideal for businesses with licensing and a defined risk appetite.

Deploy your existing developers with no special experience.

Minimum technical resources needed:

2 blockchain engineers

5-8 backend engineers

2 frontend engineers

2 dev-ops

7. Build your stablecoin experience

Implementation and rollout tips from BVNK's team of product managers and integration specialists.

Optimise your blockchain infrastructure

If you’re self-managing crypto payments infrastructure, these optimisations and automations will set you up for success. (Note: if you're using Layer1 or BVNK these features are included).

Gas management

Gas fees vary by network and processing time, and must be paid in the blockchain's native currency. Look for infrastructure that automatically calculates optimal gas fees and monitors transactions on-chain, adjusting during network congestion to prevent failed payments without manual intervention.

Error handling

Don’t rely on systems that fail silently. Choose a provider that actively monitors transaction status and automatically retries failed attempts. Look for capabilities like gas refunds for failed transactions and intelligent routing issue detection to reduce failed payouts and prevent unnecessary support escalations.

Auto-conversion

Accepting crypto is only part of the solution: converting it seamlessly matters just as much. Opt for infrastructure that supports automatic conversion into your preferred settlement currency, whether stablecoin or fiat, at the point of receipt. This ensures operational efficiency and minimizes FX risk.

BVNK's core Layer1 infrastructure automatically calculates optimal gas fees and monitors transactions on-chain

Set up your product

Plan your roll out to ensure you’re serving the right customers, with the right stablecoins and blockchains.

Support multiple stablecoins

Don't limit your reach by offering just one stablecoin. Geographic preferences vary based on local liquidity and spending options. Consider supporting popular options like USDT, USDC, PYUSD, and others.

Go multi-chain

Different blockchains suit different payment types (eg Solana for micropayments). Give users options across networks like Solana, Cardano, Ethereum, Tron, and Polygon while incentivizing use of any preferred chains.

Ensure robust fiat capabilities

Select a provider that offers:

- On/off ramping between stablecoins and fiat

- Auto-conversion to reduce exposure

- Safeguarded fiat accounts

- Access to relevant local payment rails

BVNK supports the most popular cryptocurrencies and stablecoins

Customise your front end

Boost adoption and improve conversion with these UX tips. Note: If you’re using BVNK’s hosted payments page these UX best practices are already integrated.

Optimise for mobile

With around 40% of crypto payments happening on mobile, ensure responsive design and test QR code wallet address and ‘copy’ functions across all device types.

Localize experience

Detect browser locale automatically but include a language selector option to build trust.

Prevent lost funds

- Clearly display the required blockchain network (protocol).

- Choose a partner like BVNK that can recover cross-chain transactions (and provide help centre articles like this one to advise your users on this process)

- Include destination tag prompts where required (eg for XRP payments)

Use simple language

Avoid crypto jargon and provide clear action prompts (eg "Please send this amount to this address").

Integrate popular wallets

Smooth the payment journey by integrating with popular wallets like Coinbase, MetaMask, and Trust Wallet. For stablecoin payouts, consider enabling users to create a wallet at the point of withdrawal to improve adoption among non-crypto native users.

Show local currency conversions

Display equivalent amounts in users' local currency early in the payment journey to build confidence.

Think ahead for discrepancies and errors

Configure how to manage underpayments and overpayments before launch to minimize support issues. We also recommend you ask your provider if they manage 'wrong chain' payments – automatically rerouting the payment to the correct chain to avoid loss of funds as BVNK does.

Enable VIP features

For stablecoin pay-ins, enable frequent users to create anytime wallet addresses by currency (payment channels), so they can save details in their crypto wallet and deposit more quickly in future, without repeating the full payment journey.

Display equivalent amounts in local currency early in the payment journey to build confidence.

Drive adoption with education

Train your team

Ensure support staff can handle crypto-specific questions before launch.

Customer communication plan:

- Awareness: Introduce benefits via homepage banners, emails, and in-app notifications.

- Education: Provide FAQs, tutorials, and video explainers to build trust.

- Engagement: Share success stories and optimize based on usage data.

Ensure launch compliance

Review regional guidelines for your launch markets and work with your provider to meet requirements like the UK's Financial Promotions regime for crypto assets.

Phase your roll out

Start with high crypto adoption markets or customer segments with higher crypto ownership.

8. Your implementation checklist

Ensure you've covered all key aspects before launch.

- Define your use case: Select specific stablecoin use case and test it out with our interactive demos

- Compliance plan: Review regulatory requirements for your markets and use cases

- Integration approach: Select your technical integration model

- Prototype plan: Create timeline for prototype development

- Market testing: Identify test market or user group

- Measurement: Establish KPIs for success

- Support: Establish customer support processes and training

- Risk assessment: Document potential risks and mitigations

- Launch plan: Create phased rollout strategy

Want to kick start your stablecoin strategy?

Speak to an expert