.avif)

Finance Magnates London: where are payments heading in 2023?

Last week I spoke on a panel about the trends shaping payments in 2023 at the Finance Magnates London Summit, one of Europe’s premier fintech conferences, alongside peers from Worldpay, IFX Payments, Eqwire and Nuvei. We were all in agreement—the biggest trend will be crypto payment adoption. But exactly what improvements can merchants and customers expect?

Here are some of the key takeaways from the panel discussion.

What are the current payment challenges for merchants?

The number one pain point we see, and that resonates with almost all merchants in some way, remains the impact on cash flow of late or failed payments. Cash flow is the lifeblood of any business. A late payment not only impacts cash flow; it also incurs administrative burden and cost in chasing it down. So large businesses aren’t untouched. They may have deeper pockets to shoulder a shortfall in cash flow for a while, but they are hit harder by the volume of payments they process.

Traditional payment networks offer little help. Fees from card networks and banks are taken at the point of transaction, so merchants are in the red from the start. Settlement windows can be long, more so when processing payments across borders through the Swift network where banking and FX intermediaries add more time and cost. And disputed payments will see the presumption of guilt fall on merchants, leaving them with the option to refund customers or the burden of proving their innocence.

All this, of course, depends on the payment going through at all. That is not always the case. Stricter rules on anti-money laundering and fighting fraud leaves merchants more inclined to air on the side of caution and block all dubious payments, including some genuine ones. One 2021 report suggested merchants in the US, UK, Germany and France alone lose $20.3bn at the checkout each year due to false declines. That’s without accounting for the fallout on customer loyalty and future sales. Once again, passing payments between countries compounds the problem, with inconsistencies in data standards between jurisdictions stopping payments in their tracks.

Then there’s the sheer amount of different payment methods that a customer-focused merchant must adopt—global cards, local cards, bank-to-bank, BNPL, digital wallets, prepaid cards, digital vouchers…the list goes on and seems to grow. The more markets a merchant wants to play in, the wider variety of payment methods they will need to offer. Catering for every payment preference can require significant resources to integrate new methods with current systems and to manage these effectively.

How is technology improving these payment challenges for merchants?

If you think of any payment issue that merchants face—late payments, customer preferences, processing costs, operational complexity, security—technology is helping to address them all.

APIs have been a hugely important innovation. They bring much-needed connectivity to the dislocated banking and payment ecosystem, smoothing the flow of domestic and international payments. APIs allow merchants to adopt new payment methods with relative ease and channel everything through a single platform. They also make it easier for merchants to plug in additional software capabilities to their payments stack, be it checkout optimisation or enhanced fraud management.

A profound impact of APIs has been open banking, and there is a strong case to be made that open banking payments are a huge step forward. But there is a question of commercial viability. Letting customers pay directly from their accounts is great…but only for customers. Banks aren’t making enough money from it to spark real momentum. Progress so far has largely come as a result of regulators putting pressure on banks to play ball, and only with limited application, mainly enabling payments between accounts belonging to the same customer. In truth, banks are better off with the old payment ways. So you could justifiably wonder how ‘open’ open banking will become. Without a critical mass of banks around the world really getting behind open banking payments, it is hard to see it usurping card payments.

Also, open banking does nothing to address financial exclusion. In fact, quite the opposite. It is predicated on someone having a bank account. Neither does it wholly fix other fundamental problems, such as payments with incorrect references or data formats that are incompatible between different banking systems.

Ultimately, APIs can only improve what’s there. And, ultimately, what’s there remains slow, costly, unreliable, and out of reach for millions of people around the world.

What are the emerging payment trends that merchants should be looking out for?

In the last few years, we’ve seen more and more merchants begin to adopt crypto payments, among them global household brands such as Microsoft, Etsy, Amazon, Whole Foods and Starbucks. A big driver is customer demand. A 2021 study by PYMNTS found that 93% of cryptocurrency users would consider making purchases with it. Even those without want in; 59% who have never held cryptocurrency would make purchases with it. That is a big crowd. Today there are around 220-250m owners of crypto. That is expected to surpass 1bn by 2024. Merchants that ignore this trend could be denying themselves customers.

When you consider the range of benefits for customers and merchants alike of crypto payments, and the variety of potential use cases—topping up accounts (think pensions, FX trading, gaming platforms), payouts (think employee expenses, refunds, insurance settlements) and enabling peer-to-peer lending—the drivers are there for this adoption trend to grow.

First, crypto is available to anyone with a mobile device and internet connection. Immediately that brings into scope the millions of people worldwide who are currently unserved by traditional finance and banking. Crypto payments are also fast, secure and cheap. Any specific crypto exists as a single global currency, enabling price standardisation across countries and removing the need for complex and often opaque exchanges of value. Blockchain transactions follow uniform rules and experiences, regardless of where the payment originates and ends up. Settlement is full and final, so refunds are at the discretion of the merchant and not a blanket rule that encourages fraudulent chargebacks. And crucially, blockchains operate 24/7, so merchants avoid the cash flow gap between the costs of selling and revenues from sales.

What challenges do merchants face when adopting crypto payments?

Right now it’s easy to be a bit dismissive of crypto. We’ve just had the collapse of the FTX exchange, off the back of the collapse of Terra earlier in the year. For merchants that see these stories are evidence to stay away from crypto, I’d argue they illustrate a maturing sector expunging itself of its imperfections. The underlying fundamentals of blockchain, and established crypto like Bitcoin, Ethereum and the USDC stablecoin, are not in doubt.

But equally, it’d be wrong to see crypto payments as a panacea. Price volatility is an issue, though collateral-backed, fiat-pegged stablecoins answer that. Transaction speed is also a justified criticism, though the go-to comparison of Bitcoin versus Visa (Bitcoin manages around 7 transactions per second, while Visa does 24,000) does not take account of other cryptos that use faster proof protocols.

I’d argue a bigger obstacle to crypto payment adoption is the perceived complexity of it all. Other than for crypto natives and those working in the sector, crypto can seem like a complex, murky world. Talk of nodes, proof-of-work, and custodial versus non-custodial wallets can quickly make a merchant feel out of their depth. More importantly, an uneducated consumer will also be unaware of the benefits. This inability to inspire and inform consumers has been one of the flaws of open banking.

Add to this an evolving regulatory environment, and a serious beefing up of obligations around KYC, AML and other anti-financial crime measures, and adoption for merchants can feel more risk than opportunity.

What’s the right move for crypto-ready merchants?

Merchants can learn a lot from traditional payments. Crypto aside, the last decade has seen enormous innovation in payments. Despite the issues I have described above, payments today are so much better than they used to be. Better customer experiences, more reliable processing, more cost-efficient performance, and easier access to analysis. That is almost entirely the result of the flourishing global fintech community that saw the flaws and built the solutions. It is to these fintechs that forward-thinking merchants turned, to transform their payment operations from financial afterthought to competitive advantage.

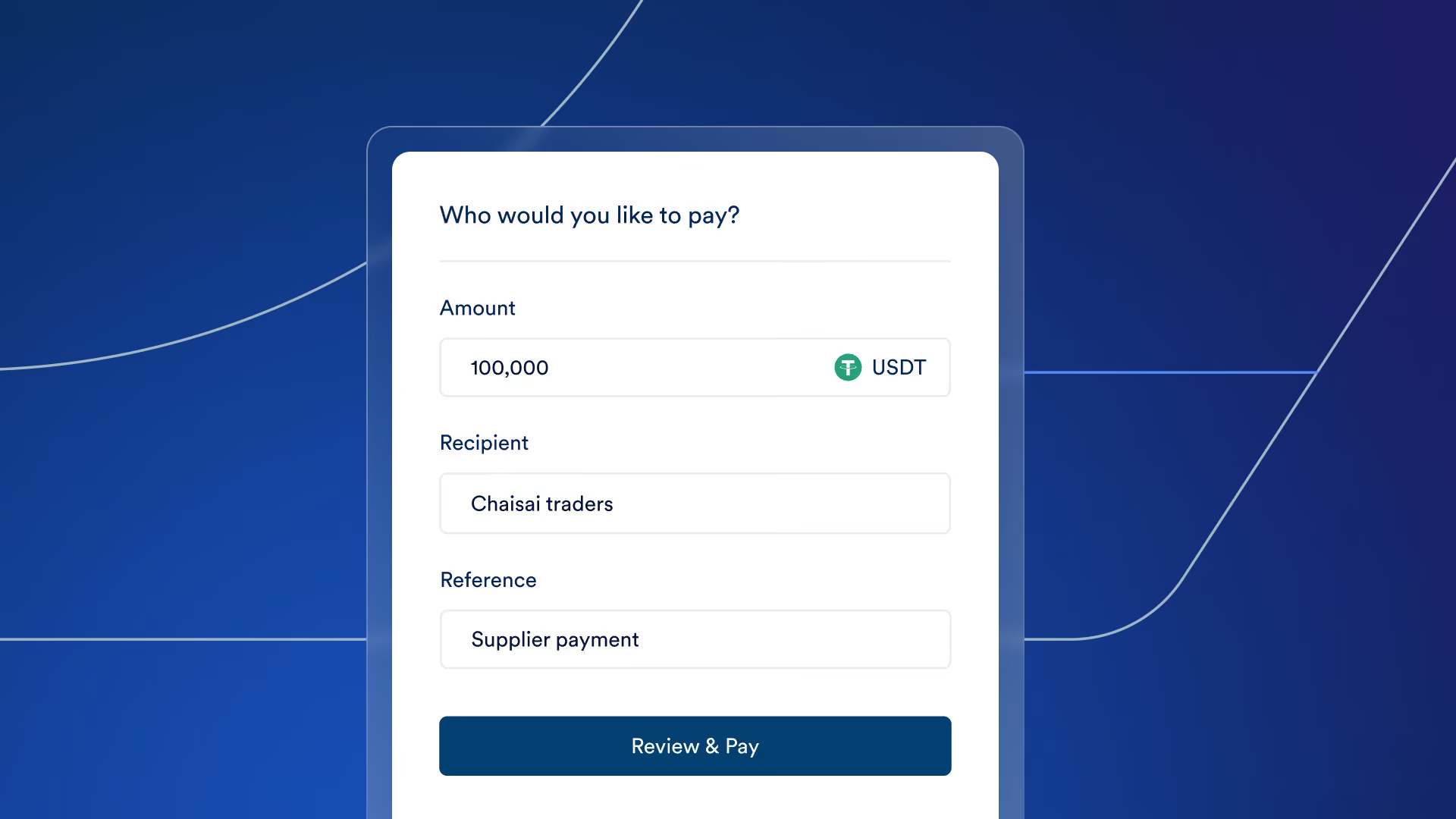

The lesson for merchants is that you don’t need to become a crypto expert to reap the benefits of crypto payments. Nor do you have to go all in at once. Being able to offer crypto at the checkout but settling in stablecoins can be a great way for a merchant to ease their way into this world without taking on an uncomfortable level of exposure. They only need the right fintech partner—with the technology, compliance systems and global relationships—to enable the capabilities.

All payments are built on trust and credibility. Crypto is no different. Customers need to feel that from their merchants, and merchants need to have that from their payment partner. They must choose wisely who to lead them on their great crypto adventure.

BVNK is a next-generation payments platform for global businesses. We bridge the gap between traditional and digital finance to make payments borderless, instant, and secure. Using the BVNK platform, businesses can send and receive payments on all major schemes and blockchain networks, incorporate stablecoins into their payment flows, and settle funds in over 30 markets.

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

Never miss an insight.