Cross-border payment solutions: how to choose the right fit for your business

.avif)

Introduction

The value of the global cross-border payments market will grow from $190 trillion today to $290 trillion by 2030, according to FXC Intelligence. Processing these payments efficiently has profound consequences for businesses. Cash flow, customer loyalty, and ultimately competitiveness are all influenced by the speed and cost of processing cross-border payments.

Today, businesses have more choice than ever about the methods they use. In this article, we will explore the leading international payment methods and some emerging alternatives, such as blockchains, and explain what your businesses should be looking for to find a cross-border payment method that suits your specific needs.

Types of cross-border payments

There are all sorts of reasons why businesses and people need to move money internationally. Some common examples include:

Ecommerce

When a customer purchases a product from an international website, they will hope to make that purchase in their domestic currency, while the merchant will want to settle the funds back in their own currency. Ecommerce is also becoming more popular in the B2B sector, and is predicted to be worth $22 trillion by 2030, making it the leading non-wholesale B2B channel for international payments. A large portion of those transactions will be taken by online B2B marketplaces, such as Alibaba, Amazon Business, Upwork, ECPlaza.

Remittances

People living and working abroad often send money back home to their families. Cross-border payments enable them to do so more quickly and securely than sending cash or cheques in the post.

International trade

Businesses that import or export goods need to make cross-border payments to pay for the products they buy, or receive payment for the products they sell. This includes fees for agencies and freelance staff, and subscriptions for software services.

Travel

When abroad, people will be making cross-border payments for things they purchase.

Business payouts

Businesses will need to make payments to individuals in a different country, such as paying wages, settling insurance claims, and processing refunds. They also need to make payments to third-parties in other countries that are involved in their business, (sometimes known as invoice payments), such as paying suppliers or paying commission to sellers trading via a marketplace.

Trading platforms

Companies that trade on financial markets (eg FX, stock exchanges, crypto platforms) will need to move and convert large volumes of currencies to execute positions. When people use online trading platforms that operate from a different country they will typically deposit funds to execute a trade.

Treasury flows

To meet operational and regulatory liquidity requirements, a multinational company's treasury department will need to move money around its organisation. International businesses will also have separate legal entities and bank accounts in most, if not all of the markets they sell into. At some point, they will want to repatriate these foreign funds to their domestic bank or between different legal entities in their business structure.

Typical challenges of cross-border payments

To choose the right cross-border payment method(s), businesses must be aware of the general challenges of moving money internationally.

Dislocated networks

Banks do not operate within a single, standard network. Instead, international banking is characterised by multiple networks around the world, working to different standards and rules. To move money internationally, different networks may need to interact, and intermediary (or ‘corresponding’) banks used to pass money through them. This complexity adds time and cost to a cross-border payment.

Incompatible data

Banking jurisdictions around the world use different data standards and formats, making the payment instruction message between them illegible. This can lead to payments being refused. This is set to improve with the adoption of ISO 20022, a new global standard for electronic data interchange between global financial institutions; but that is only now being adopted by banks and financial institutions.

Burden of regulation

Compliance, security protocols, and national capital controls are other variations between banking jurisdictions that can complicate the path of a payment, or even stop it in its tracks.

Availability

Most banks around the world still operate on a 9-5 basis, which means that money being sent abroad may have to wait until the following day (or days for weekends and public holidays) before the payment can be completed.

Outdated technology

Most banks have resisted upgrades to their core banking platforms and still rely on outdated functionality (such as daily batch processing) and manual or semi-automated processes.

What to look for in a cross-border payments solution

Done well, cross-border payments can help to open up new markets, create operational efficiencies, and improve cash flow. Here are some key criteria that businesses should consider when choosing their optimum cross-border payment methods.

Operational simplicity

Cross-border payments that are difficult to set-up and administer suck up valuable resources and budgets. Conversely, payments that can be adopted and automated save time and money, which can be redeployed back into the business or passed on to the customer through lower prices.

Fast settlement

Fast settlement times ensure a business retains money on its balance sheet for longer; while shorter settlement windows reduce the fluctuations in exchange rates between the moment of transaction and settlement. Settlement and cash flow is important for all businesses, but more so for SMEs that tend to have more precarious liquidity and tight margins.

Regulation and compliance

Every payment method is subject to some level of regulation. While some obligations are well-understood and can be (broadly) automated (eg KYC, AML), others payment methods have less mature regulatory frameworks, such as blockchain-enabled payments that use cryptocurrencies. While on the surface this may be perceived as an advantage of having less to do, it does leave businesses and their customers more exposed to risks, and needing to be agile to adopt regulations when they get introduced. Payments partners play an important role in sharing the burden of compliance.

Data transparency

Information about cross-border payments is key to enabling effective tracking and long-term financial planning. Data around fees, processing times, progress to settlement, and reasons for payment failures are essential for making informed choices about your payments operation.

Risk and resilience

The ultimate test of a payment method is whether it works, and that the money is safe in transit. Technological resilience can be taken for granted; the big international banking networks, card networks and blockchains have been proven over many years. Rather, businesses should be looking at payment success rates (ie the amount of genuine payments that are initiated that are successfully completed.) Payment methods with high levels of fraud can cost merchants in chargeback rates, while systems with enhanced security protocols (eg Strong Customer Authentication and 3D Secure 2.0) can add friction and block genuine payments. Businesses should have a clear view of their risk appetite.

Customer experience

In today’s digital world of hyper-convenience, customers want to pay with their preferred method; 60% of ecommerce consumers will abandon their cart if they cannot pay with their preferred payment method. Payers also want simplicity. Customers who are faced with friction at the checkout, opaque costs, or concerns over security may decide not to go through with the transaction, or not return.

Finding the right cross-border payments solution for your business needs

Swift

Swift (Society for Worldwide Interbank Financial Telecommunication) is the dominant method for processing cross-border payments. Swift is used by more than 11,000 member institutions. They include all sorts of financial organisations that need to move money internationally — banks; brokerages and trading houses; securities dealers; asset management companies; clearing houses; depositories; remittance services; and non-financial businesses. Collectively they send an average of 44.8 million payment messages daily through the network. The benefits of Swift include its global scale and trusted technology, while it has also rolled-out new innovations in recent years, such as Swift gpi. But Swift also has flaws, including opaque fee structures, slow settlement times, technical complexity and political influences. Read more about Swift.

Other banking networks

Global ACH (also called International ACH Transfer) is a method for moving money between US and foreign bank accounts, using other country payment rails including EFT, SEPA, BACS and BECS. SEPA (Single Euro Payment Area) is a dominant international banking network in Europe. Domestic banking networks can also be used in combination to process international payments, such as Fedwire (US), CIPS (China), BACS (UK), BECS (Australia) and EFT (Canada). India and Singapore have recently linked their digital payments systems, UPI and PayNow, to enable instant and low-cost fund transfers, with customers from eight banks able to benefit.

Card networks

International card networks (eg Visa, Mastercard, Amex) are popular ways for businesses to process payments from foreign customers. Card payments using these networks can be a good option for cross-border transactions as they are widely accepted, convenient and secure. They are becoming more important in the B2B sector as more commerce there moves online. They can also incentivise businesses to buy more through reward and protection schemes. However, card transactions may be subject to currency conversion fees and other charges, and because they leverage banking networks like Swift to move money, they share some of the same issues such as slow settlement.

Blockchains and cryptocurrencies

A blockchain is a shared database, or ledger, distributed among nodes on a computer network. It is separate from traditional banking and card networks (and solutions that use those systems), and so is not subject to their operating times and geographical constraints. A blockchain is territory agnostic, with a single currency and transparent protocol for every user, wherever they are in the world. Users on a blockchain can pay each other directly, eliminating the need for third-parties, and so minimising cost and settlement times.

For these reasons, cryptocurrency payments are most popular in emerging markets, where financial exclusion tends to be higher. Of the top 20 countries where cryptocurrencies are most widely used for payment, ten are lower middle income (Vietnam, Philippines, Ukraine, India, Pakistan, Nigeria, Morocco, Nepal, Kenya, and Indonesia); eight are upper middle income (Brazil, Thailand, Russia, China, Turkey, Argentina, Colombia, and Ecuador); and two are high income (United States and United Kingdom).

Blockchains are a proven technology for securely transacting; in the B2B sector alone, blockchain-enabled cross-border payments are expected to exceed $4.4 trillion by 2024.

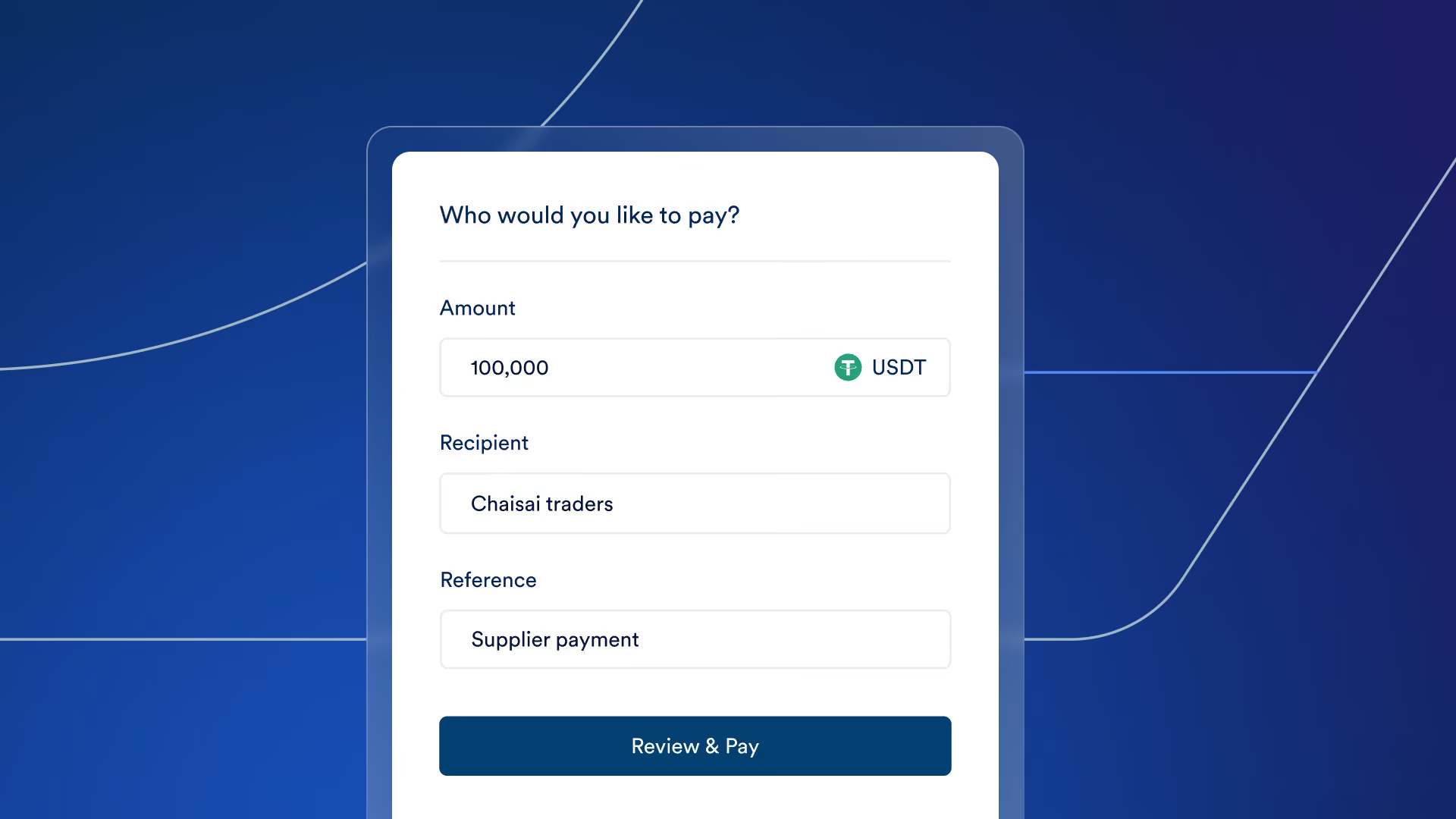

That said, the cryptocurrencies that run on them (eg bitcoin) are largely unregulated and their value can be relatively volatile. Stablecoins, which peg their value to a fiat currency, fix the volatility issue; and with collectively over $40 billion of trades made every day, is a proven technology. The largest stablecoin is Tether USD (USDT), which is pegged to the US dollar. It has a market cap of around $83 billion.

Central Bank Digital Currencies (CBDCs) are another crypto alternative to enabling cross-border payments using blockchains. They are issued by central banks, and so provide greater regulatory protection. There are now over 100 CBDC projects around the world in various phases of development and testing.

Blockchains and cryptocurrencies can also be used to process fiat currency payments efficiently. The payer ‘on-ramps’ with a fiat currency, which is then converted to a cryptocurrency (typically a stablecoin) that is transferred across the blockchain before being converted and paid out in the payee’s preferred fiat currency.

Leading providers of blockchain cross-border payments include BVNK’s Global Settlement Network and Ripple/XRP.

FAQs

What is the fastest cross-border payments method?

The fastest cross-border payment method will depend on a range of factors, such as the transaction amount, and where you are moving money to and from. In many cases, blockchain-enabled payments, such as stablecoins, are fastest because they are completely separate from legacy banking rails. Blockchain payments usually settle within 24hrs, and sometimes in just minutes or seconds. Blockchain payments in particular benefit international payments involving uncommon currency pairs and emerging countries, where the use of traditional banking networks would require multiple corresponding banks. Moving smaller quantities of money between countries using established banking networks (eg Swift, SEPA) will tend to be faster, and sometimes within hours.

What is the best payment method for international business?

The best international payment method depends on your priorities. International banking networks (eg Swift, SEPA) are trusted, but can be slow and expensive depending on the transaction amount, and where you are moving money to and from. Card payments are easy for most customers to access, but can attract costly processing and FX conversion fees. Blockchain payments operate 24/7, and stablecoins get over the issue of price volatility. But cryptocurrency regulation is in its infancy and evolving, and so carries balance-sheet risk.

How big is the cross-border B2B payments market in 2023?

The value of the overall global cross-border payments market will grow from $190 trillion to $290 trillion by 2030, according to FXC Intelligence. Of that, B2B payments will grow from $39.3 trillion to $56.1 trillion in the next seven years.

What are the leading payment methods for cross-border transactions?

Popular payment methods for cross-border transactions include Swift, credit and debit cards, fintech networks, and blockchain and cryptocurrencies, including stablecoins.

What is Swift?

Swift (the Society for Worldwide Interbank Financial Telecommunications) is the primary network for moving money internationally, with 11,000 member institutions worldwide and facilitating $150 trillion in transactions per year.

What are the challenges of making cross-border payments today?

Some of the challenges of making cross-border payments include: dislocated banking networks; incompatible data standards; different regulatory jurisdictions; and the limited availability of banking systems.

What should businesses consider when choosing the right cross-border payment solution?

When choosing their optimum cross-border payment methods, business should consider a number of factors, including: operational simplicity and interoperability with other financial systems; speed of settlement; processing costs and other fees; access to information and insights; the customer experience; and their attitude to security.

How many B2B cross-border payments are made using blockchains?

Juniper Research estimates that B2B cross-border payments made on blockchains will account for 11% of the total B2B international payments by 2024. A 2021 study by PYMENTS found that 93% of cryptocurrency users would consider making purchases with it; anf that 59% of people who have never held cryptocurrency would also make purchases with it.

What should I consider when deciding on a partner to support my business with cross-border payments?

When selecting a payment provider to support your business with cross-border payments, you should consider their global coverage, breadth of capabilities, ease of deployment, processing times and fees, technical support, and compliance.

Conclusion

Today, businesses have more choice than ever about the cross-border payment methods to adopt. No one method is perfect and some methods may be more suitable for certain markets and territories. The key for businesses is to continually test, and use data insights to adapt their cross-border payment strategies.

Enterprise businesses that operate in multiple markets and with deep resources have the need and means to use different payment methods in parallel. This will be more challenging for SMBs, but some experimentation should still be possible.

That said, running more payment methods can add complexity and cost to a payments function. So some level of balance is needed. Fintechs and third party partners that can orchestrate and automate cross-border payments will become increasingly helpful. That creates a second challenge for businesses, namely how to choose the right cross-border payments partner. The selection criteria should be far-reaching and prioritise global coverage, breadth of capabilities, ease of deployment, support, and costs.

BVNK is a next-generation payments platform, trusted by hundreds of businesses globally to process billions of dollars in payments every year. We bridge the gap between traditional and digital finance to help merchants reap the benefits of blockchain-enabled payments with minimal risk and technical setup.

We enable businesses to move money around the world without needing to interact with the Swift network, accept payments in cryptocurrency from their customers in checkout without having to hold crypto or change their treasury operations, and embed crypto and stablecoin solutions into their products and services without needing to become regulated.

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

Never miss an insight.