.avif)

Cross-border payments: challenges and trends in 2023 and beyond

Introduction to cross-border payments

Businesses have well understood the benefits of optimising payments. They include a better customer experience, higher checkout conversion, lower operating costs, and improved cash flow. As such, payments have become a frontier for creating competitive advantages.

When applied to cross-border payments, where there is greater potential for growth, these benefits become scalable. Likewise, so do any inefficiencies.

Businesses and their customers can be underserved by the legacy infrastructure that processes most cross-border payments. For certain markets and tasks, new technologies and fintech services are offering better ways to move money. Businesses that adopt them can save time, money, and create superior experiences for their customers.

Exploring these opportunities is a gradual process. Legacy payment infrastructure is too entrenched and trusted to be dismissed. Rather, we are entering a period of coexistence between traditional and new cross-border payment methods.

In this guide, we’ll explain the hidden costs in the way most cross-border payments are processed today. We’ll also explore the leading alternatives and the gains a business can expect by adopting them.

Why are cross-border payments important?

The value of the global cross-border payments market will grow from $190 trillion today to $290 trillion by 2030, according to analysts FXC Intelligence. Behind those numbers are stories of businesses expanding into markets, new inwards flows of investment, and migrants sending money back home. With that comes more consumer choice, more jobs, and higher returns for shareholders.

But progress is not inevitable. How money moves between banks in different countries is a key factor. Do that quickly and at low cost, and businesses get the capital they need, when they need it. But when you’re waiting to receive money that is due to you, and when banks and third-parties levy fees or take a cut for their part, commerce goes slower. As cash gets tied up in the system, cash flow suffers. With less working capital, businesses become less competitive, while consumers wait to get paid or receive money from abroad.

This is what happens today.

So far, this has been a challenge for the wholesale banking and business-to-business (B2B) sector, which accounts for 98% of cross-border transactions. But every sector stands to gain by improving how international payments are processed, including consumer-to-business (C2B) payments such as cross-border ecommerce and offline tourism; business-to-consumer (B2C) payments, such as salaries, payouts, and dividends; and consumer-to-consumer (C2C) payments, such as international remittance payments.

Common cross-border payment use cases

There are all sorts of reasons businesses and people need to move money internationally. Some common examples include:

Ecommerce

When a customer purchases a product from an international website, they will hope to make that purchase in their domestic currency, while the site will want to settle the funds back in their own currency.

Remittances

People living and working abroad often send money back home to their families. Cross-border payments enable them to do so more quickly and securely than sending cash or cheques in the post.

International trade

Businesses that import or export goods need to make cross-border payments to pay for the products they buy, or receive payment for the products they sell.

Travel

When abroad, people will be making cross-border payments for things they purchase.

Business payouts

Businesses will need to make payments to individuals in a different country, such as paying wages, settling insurance claims, processing refunds. They also need to make payments to third-parties in other countries that are involved in their business (sometimes known as invoice payments), such as paying commission to sellers trading via a marketplace, or fees of agencies and freelance staff.

Trading platforms

When people use online trading platforms that operate from a different country (ie shares, currencies, crypto) they will typically deposit funds to execute a trade.

Corporate treasury flows

International businesses will have separate legal entities and bank accounts in most, if not all of the markets they sell into. At some point, they will want to repatriate these foreign funds to their domestic bank or between different legal entities in their business structure.

Cross-border payment methods

Many familiar domestic payment methods (eg credit cards, bank transfers, cryptocurrencies) can be used to make a cross-border transaction. Here are the leading payment methods.

Cards

Credit cards and debit cards are popular ways for businesses to take payments from foreign customers, and can also be used for making international B2B payments. Card payments can be a good option for cross-border transactions as they are widely accepted, convenient and secure. They can also incentivise shoppers to buy more through reward and protection schemes. However, card transactions may be subject to currency conversion fees and other charges.

Wire transfers

A wire transfer (also known as a bank-to-bank payment or bank transfer) is an electronic transfer of funds, usually processed via a banking network. When funds are moved between banks in different countries, it can be called ‘correspondent banking’. Swift (the Society for Worldwide Interbank Financial Telecommunications) serves as the primary network for moving money internationally, with 11,000 member institutions worldwide and facilitating $150 trillion in transactions per year.

SEPA (Single Euro Payment Area) is a dominant international banking network in Europe. Domestic banking networks can also be used in combination to process international payments, such as Fedwire (US), CIPS (China), BACS (UK), BECS (Australia) and EFT (Canada). India and Singapore have linked their digital payments systems, UPI and PayNow, to enable instant and low-cost fund transfers, with customers from eight banks able to benefit.

International wire transfers are relatively secure, though genuine transactions can get caught by enhanced security protocols designed to stop fraudulent or illegal activity. Payments usually take 2-3 working days, but can take 4-5 days for more complex payment routes where more banks are involved. Banks often charge a flat fee for wire transfers, which can range between $15 and $50. This becomes a bigger problem when making low value transactions. Banks can also impose limits on the amount of money sent in one transaction.

Global ACH

Global ACH (also called International ACH Transfer) is a method for moving money between US and foreign bank accounts, using other country payment rails including EFT, SEPA, BACS and BECS. Global ACH tends to be less expensive than traditional wire transfer networks, but can take longer at around 3-4 days.

Fintech networks

Fintechs layer services on top of banking networks to solve some of the traditional challenges of moving money internationally for their customers. Examples of these services include pre-funding to simulate 'instant' payments; automatic rerouting of payments to identify the fastest and most effective settlement path; real-time information about the progress of the payment; ease of integration with other services, such as FX; management of compliance obligations; and enhanced customer support. A fintech provider allows businesses to offload much of the work involved in processing cross-border payments, allowing them to redeploy resources to core activities. Leading fintech providers of cross-border payments include PayPal, Stripe and Wise.

Blockchain and cryptocurrencies

A blockchain is a shared database or public ledger, distributed among 'nodes' on a computer network. It is separate from traditional banking and card networks, and so is not subject to their operating times and geographical constraints. A blockchain is territory agnostic, with a single currency and transparent protocol for every user, wherever they are in the world – though there are different blockchains with different native currencies. Users on a blockchain can pay each other directly, eliminating the need for third parties, and so minimising cost and settlement times. Though blockchains are a proven technology for securely transacting, the cryptocurrencies that run on them (eg bitcoin) are largely unregulated and their value can be volatile.

Stablecoins, which peg their value to a fiat currency, fix the volatility issue. The largest stable is Tether USD (USDT), which is pegged to the US dollar. It has a market cap of around $83 billion. Blockchains and cryptocurrencies can also be used to process fiat currency payments efficiently, particularly across borders. The payer ‘on-ramps’ with a fiat currency, which is then converted to a cryptocurrency (typically a stablecoin) that is transferred across the blockchain before being converted and paid out in the payee’s preferred fiat currency.

Cross-border payments companies to know about

There are a wide range of companies that can support you with processing cross-border payments. Here are some of the leading ones.

Wise

Wise is an online payments company that provides international money transfer services, including bank transfers, debit and credit card payments, local payments and currency exchange. The company also provides real-time tracking of payments and notifications of incoming payments.

Airwallex

Airwallex is used by small to medium-sized businesses to make and receive payments in over 50 currencies in more than 130 countries.

Ebury

Ebury specialises in international cash management solutions including cross-border payments, FX risk management and business lending. They work with over 49,000 businesses and organisations across Europe, Canada, Australia, UAE, and Hong Kong.

dLocal

Local is a global payment platform that enables businesses to accept payments and make payouts. It provides a single platform for merchants to reach billions of consumers in over 20 countries across Latin America, Africa, and Asia. dLocal offers over 300 local payment methods, including credit and debit cards, bank transfers, cash payments and digital wallets.

Stripe

Stripe is one of the world’s largest online payment processing platforms, enabling cross-border payments across 120 countries.

BVNK

BVNK is a global payments platform for businesses. Our Global Settlement Network enables businesses to settle funds anywhere in the world under 24 hours and seamlessly trade between currencies. We use distributed ledger technology (DLT) to replace RTGS and SWIFT infrastructure, connecting local payment schemes around the world together.

Ripple

Ripple is a peer-to-peer decentralised platform that allows for a seamless transfer of money in any form, including fiat currencies (eg dollars, yen, euros) and cryptocurrencies (eg bitcoin, litecoin). It uses its own token (XRP) to facilitate quick conversion between different currencies.

EVO Payments

EVO Payments is a global payment technology and services provider. It facilitates a wide range of international payment solutions, including credit and debit card processing, digital wallets and mobile payments.

Flywire

Flywire is a global payment, receivables and currency exchange provider that specialises in fulfilling complex international payments for businesses, educational institutions, and healthcare providers.

Global Payments

Global Payments is one of the largest payment processing companies in the world. It processes over one-billion transactions globally and supports over 140 separate payment methods.

Corpay

Corpay is a leading global payments provider for businesses, offering comprehensive cross-border payments and currency risk management solutions. They partner with more than 100 correspondent banks and counterparty trading institutions in six continents.

Challenges of cross-border payments

Dislocated networks

The international banking network is not a unified ecosystem operating to common standards, but instead a random patchwork of relationships, some more established than others. For currency pairs with high volumes of payments (eg US dollar and British pound sterling), the corresponding domestic banks are likely to have a direct relationship, making it easier to move money between them. Where this is not the case, ‘correspondent’ banks act as intermediaries. The more correspondent banks, the longer the transaction will take, and the more it will cost as each party takes a processing fee. Or the incentive to move money faster can come at the expense of fees, as banks cover their obligation to provide funding in advance of settlement. In some cases, a cross-border payment can take several days and can cost up to 10 times more than a domestic payment.

Incompatible data

Banking jurisdictions around the world use different data standards and formats, making the payment instruction message between them illegible. This can lead to payments being refused. This is set to improve with the adoption of ISO 20022, a new global standard for electronic data interchange between global financial institutions.

Burden of regulation

Compliance, security protocols and national capital controls are other variations between banking jurisdictions that can complicate the path of a payment, or even stop it in its tracks.

Availability

Most banks around the world still operate on a 9-5 basis, which means that money being sent abroad may have to wait until the following day (or days for weekends and public holidays) before the payment can be completed.

Outdated technology

Swift is a 30-year-old banking infrastructure that relies on a complex chain of intermediaries. Meanwhile, most banks have resisted upgrades to their core banking platforms and still rely on outdated functionality (such as daily batch processing) and manual or semi-automated processes. These challenges can create profound issues for businesses.

Operational complexity

Cross-border payments can be more complex and time-consuming, requiring businesses to have the necessary resources and expertise to manage them effectively.

Settlement and cash flow

A combination of expensive processing fees and long settlement times can create significant pressure on liquidity, while a business can also lose out to fluctuations in exchange rates between the moment of transaction and settlement.

Complex regulatory and compliance processes

Ever-evolving financial and data regulations are continually evolving and differ around the world, making it challenging to understand and adhere to compliance obligations.

Lack of transparency

Information about cross-border payments can be difficult to surface. This includes fees, processing times, progress to settlement, and reasons for payment failures. As such, it can be difficult to make informed choices.

Poor customer experience

Customers who are faced with friction at the checkout, opaque costs or concerns over security may decide not to go through with the transaction, or not return. And if their preferred payment choice is not available, they may not even start.

Benefits of cross-border payments

Done well, cross-border payments can provide a range of benefits to businesses. By being able to send payments quickly and securely across borders, companies are no longer constrained by physical location, allowing them to tap into new markets with potentially huge rewards.

Opening new markets

By having access to a wide range of payment methods, companies can expand into new markets and gain more customers while providing better services. By offering customers a more convenient and reliable payment experience, businesses can expect to not only increase sales, but also build long-term customer loyalty.

Increased efficiency

By streamlining processes and reducing transaction times, businesses can save time and money that would otherwise be lost on unnecessary delays or admin. This increased efficiency also results in less foreign exchange risk and often also improved customer service, as payment processing becomes faster and simpler.

Cost savings

Companies can often save money by taking advantage of better exchange rates or lower fees when processing cross-border payments. This cost saving can then be reinvested back into the business or passed on to consumers in the form of lower prices, both of which help to boost profits.

Cash flow

One outcome of lower processing costs is improved cash flow. Businesses can also improve their cash flow by selecting cross-border payment methods with fast settlement times.

How blockchain improves cross-border payments

For some tasks, distributed ledger technology (DLT) like blockchains and digital assets like cryptocurrencies are an effective alternative to make cross-border payments faster, safer, and less expensive.

Attract customers

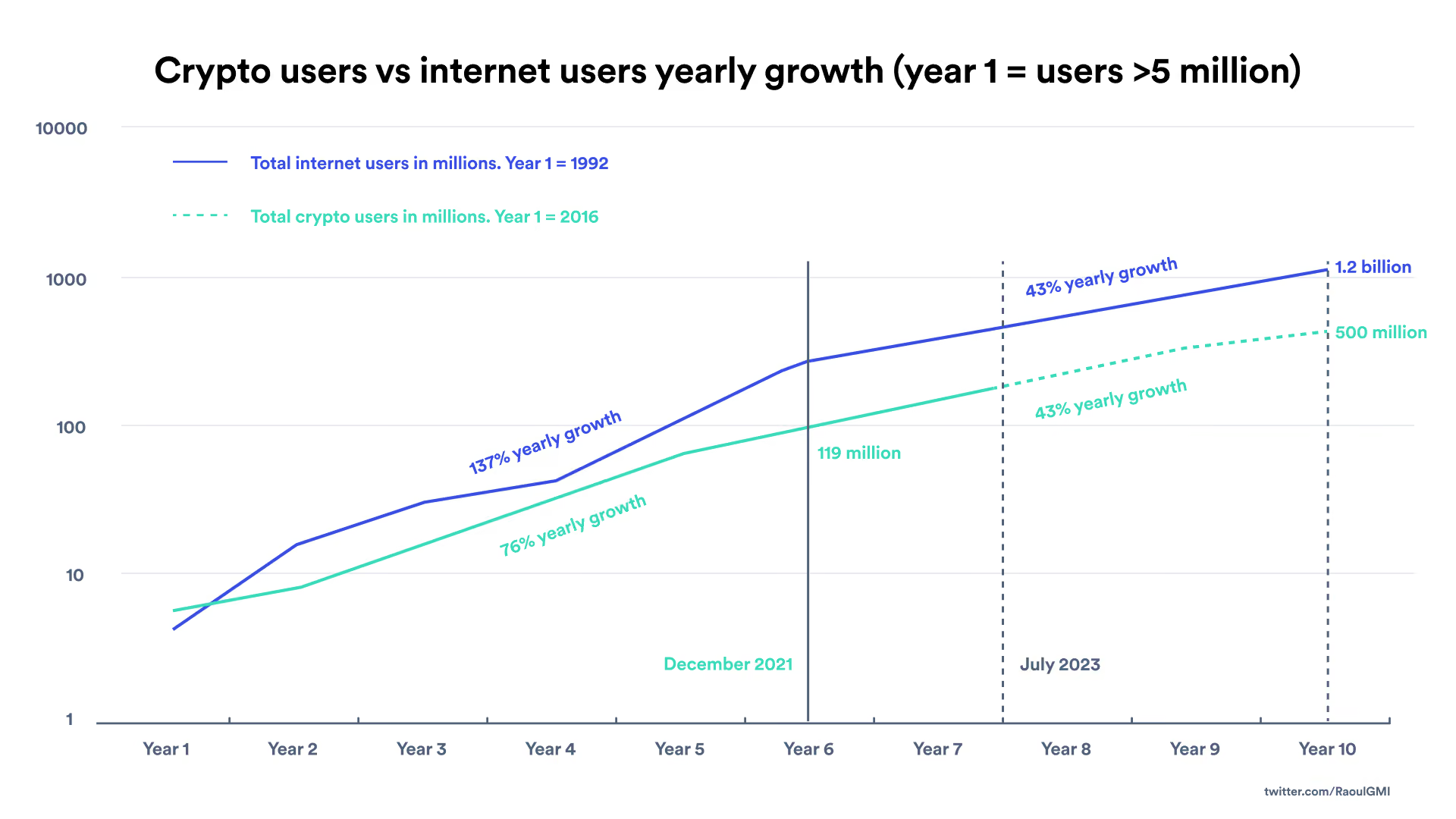

There are an estimated 420 million owners of cryptocurrency globally, and some estimates suggest this could reach 1 billion by the end of 2025. There are around $1.3 trillion of cryptocurrencies in circulation in 2023 and while adoption has slowed from its 2021 peak, the trajectory is clear. A study by PYMNTS found that 93% of cryptocurrency users would consider making purchases with it. Even those without plan to adopt it; 59% who have never held cryptocurrency would make purchases with it. By offering it as a payment method, businesses can reach new markets and demographics, especially where traditional banking is hard to access or local market currencies suffer from inflation.

Speed up settlement

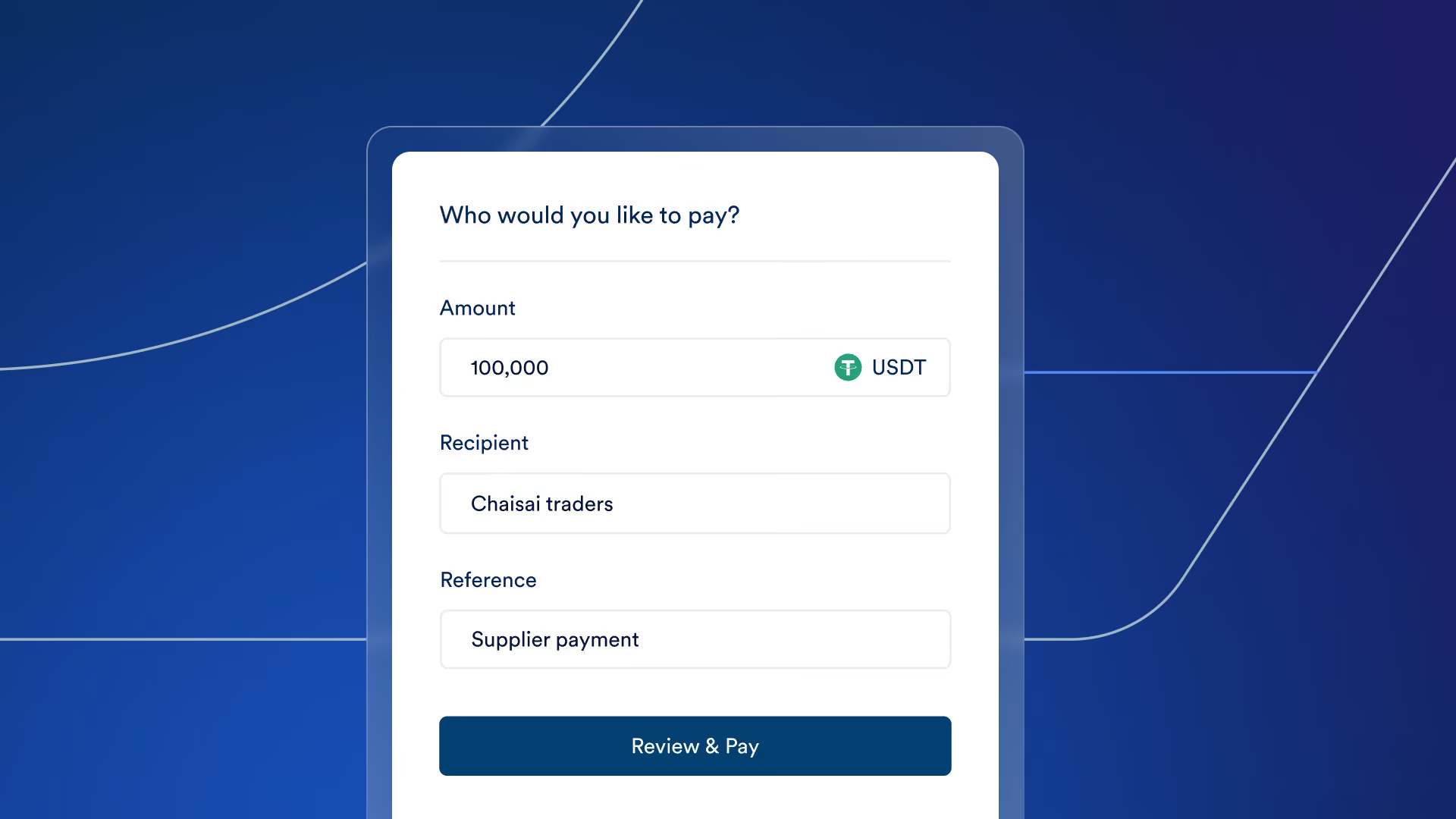

Moving money quickly across borders is difficult. Depending on the number of banks involved, it can take up to 5 days using Swift. With blockchains, funds settle faster, easing cash-flow. Settling a payment on a blockchain takes just minutes, though many businesses will still want to convert into fiat currency (known as ‘off-ramping’). This part of the transaction involves banks, so adds on time. Times vary by provider, but as an example BVNK settles payments through our Global Settlement Network within 24 hours.

Lower costs

Businesses pay a high price to process cross-border transactions using the international banking system. As we have read, the more complex the payment route between two countries, the more costs will be incurred. Businesses could save up to 80% on foreign exchange fees, according to some studies. If you’re converting in and out of fiat currencies though, also known as 'on- and off-ramping', there are additional costs involved. But you could still achieve savings, depending on the provider and currencies involved.

Fight fraud

Blockchain settlements are full and final, with no facility for customers to request chargebacks, therefore eliminating erroneous chargebacks requests and friendly fraud. Blockchains are also transparent. Blockchain ledgers are also highly transparent. Each transaction has a unique identifier, assigned when the transaction is started and is completely visible, permanent and auditable. This gives payments and compliance teams powerful new ways to monitor transactions, track the flow of funds and prevent illicit activity.

Security

Blockchains are a proven technology for securely transacting and recording small and large amounts of crypto every day. Cryptocurrencies & blockchains use encryption to make transactions anonymous and secure. Using blockchain cryptography, two parties can complete a transaction without sharing their own information or having to use a middle man such as a bank or government. Different types of encryption include: symmetric encryption, asymmetric encryption, and hashing.

Easy to deploy

An entire blockchain-enabled payments operation can be outsourced to a third party, giving a business all the benefits of offering crypto payments to their customers with none of the risk or compliance obligations of holding crypto assets on its balance sheet.

Stable

Critics of blockchain-enabled payments point to the volatility of cryptocurrencies as a flaw. Using stablecoins can overcome this. Payments can be collected in either a cryptocurrency or fiat currency and instantly converted to stablecoins. Stablecoins can then be converted into the settling currency or held as a long-term asset on the balance sheet, therefore nullifying the risk of currency conversion. BVNK’s cross-border payment solution — Global Settlement Network — can process up to EUR10m in a single payment transaction for enterprise clients.

Choosing the right cross-border payment strategy and partner for your business

Businesses looking to refresh their cross-border payment strategy have lots to consider.

They should start by deciding how ‘local’ they want to go with payments. Markets around the world are very different regarding payment preferences, technological and commercial maturity, and regulations. A ‘one-size-fits-all’ approach is inadvisable, but equally being too tailored will be inefficient and unworkable. Understanding the potential of each market and their similarities can help you find the right balance.

You’ll then want to consider operational elements, such as enabling the right technology; creating the perfect customer experience; maintaining the regulatory know-how; and continually staying on top of innovations and rule changes. That can quickly suck up resources.

That’s why many companies decide to offload complexity to experts, leaving them to focus on their core business activities.

But what partner should you choose? Here are some factors you should consider when choosing a cross-border payments solution and partner to support your business with cross-border payments.

Coverage

Select a payment provider that has a global reach but can also accommodate local market customisations. As a start they should have all the necessary licences, memberships or regulatory coverage to acquire and process payments in each of your markets. They should also be able to offer a good range of international and local card brands, bank transfers, e-wallets, e-cash, mobile, and crypto payments.

Breadth of capabilities

A mature cross-border payments operation is not simply about moving money from A to B. It’s also about the checkout experience, managing fraud, optimising settlement times and costs, access to data and insights, and complying with regulations. It can be more efficient to get all these capabilities within one platform, though not at the risk of access to best-in-class tools and operational resilience.

Ease of deployment

APIs and plug-and-play services make it easy to get started with a partner, integrate third-party solutions, and scale. Look for compatibility with your website, mobile apps, or point-of-sale (POS) systems. Seamless integrations will make the payment process smoother for your customers.

Processing times and fees

Have a clear understanding of how a payment partner makes their money, and the SLAs they commit to in terms of settlement times. Both of these have a profound impact on cash flow.

Technical support

Cross-border payments are a highly technical exercise, and you should have immediate access to support to fix things when they go wrong. Look for support teams in each of your major markets, so you get round-the-clock support.

Compliance

Though typically a payment partner will take on the burden of regulatory compliance, your business could still be liable. Look who’s in their compliance team; if they have detailed governance and oversight framework that clearly articulates policies and procedures; and how compliance is embedded throughout the solution.

The evolution of cross-border payments

A number of trends are changing how businesses approach cross-border payments.

Customer expectations

Consumers and business customers are less willing to accept the inconvenience and cost of traditional payment rails. Alternative solutions that offer faster, cheaper, and more transparent cross-border payment solutions are more in tune with the digital expectations of customers.

Changing macro trends

Emerging markets in Africa, Latin America, and Asia are hotbed of progress. This is partly driven by need. These countries have high proportions of people who have been excluded from traditional banking and financial services, or whose domestic currency suffers from hyperinflation and capital controls. Record levels of migration have also created more demand for better ways to move money internationally, while also migrating popular payment methods themselves to new territories. Cross-border remittances are expected to grow to $1.1tn by 2025, more than double what they were in 2010. That is being led by intra-European remittances, aided by the SEPA banking network.

It is also driven by policy. Initiatives such as the African Continental Free Trade Area and China’s Belt and Road Initiative are opening up trade to these parts of the world. In contrast, the UK and EU are grappling with the impact of Brexit, the US has adopted a more protectionist stance in recent times, while sanctions rewrite established trade alliances. Emerging markets are also benefiting from mobile phone ownership and mobile payment solutions. Of the top 10 countries with the highest mobile penetration, eight are considered emerging markets (China, India, Indonesia, Brazil, Russia, Nigeria, Mexico, and Pakistan).

Provider incentives

These trends and pains have ushered in new cross-border payments fintechs, looking to provide fixes. Some work alongside incumbent banking systems to improve them, while others are creating entirely distinct payment rails such as DLTs and blockchain payments. Despite much innovation in this space in the last decade, no fintech has more than 1% of market share globally, signaling a huge opportunity for them to gain share.

Meanwhile, the incumbents are not about to relinquish their share of international payments. Swift has been innovating — new services such as Swift Go and pre-payment validation saw its payment volumes increase by 11% in 2021, while it is also looking into Central Bank Digital Currency CBDCs as a means for processing cross-border payments. Visa is exploring using the stablecoin USD Coin (USDC) and the Ethereum network for global settlements, while Amercian Express has been working with Ripple since 2017 to process blockchain-enabled international B2B payments.

All this is good news for businesses and their customers. More competition will spur innovation and increase choice. Users will become more discerning, and providers will have to fight for market share on multiple fronts, including settlement times, cost, and UX. These are strong areas for DLT and blockchain payments, and consequently more providers will look to develop their own DLT payment solutions, or leverage established providers such as BVNK and Moneygram’s partnership with Stellar.

Growth across all sectors

Cross-border payments will increase across every sector; but most profoundly in the B2B ecommerce market, which is due to grow by 120% between 2023-2030 to be worth $21.9tr. This reflects the digitisation of the B2B market, which has until now lagged behind B2C. Other sectors are also set to grow rapidly.

.avif)

Changing regulation

When it comes to DLTs and cryptocurrencies, regulation will be an increasing focus. For all the benefits of blockchain cross-border payments (eg fast, low cost, secure, accessible) the technology still wrestles with a perception problem of risk. That is being addressed. The European Union has already agreed on a provisional version of the Markets in Crypto Assets (MiCA) framework, which will be the most substantial piece of crypto regulation yet when it comes into effect. The UK has added crypto to the scope of the proposed Financial Services and Markets Bill, which already seeks to extend payments rules to stablecoins. In parallel, the Bank of England is developing a CBDC wallet to execute payments. In Asia, the Monetary Authority of Singapore (MAS) recently published two consultation papers proposing regulatory measures for crypto, one directed at mitigating risks of consumer harm from cryptocurrency trading, and another to support the development of stablecoins as a credible medium of exchange.

Despite the benefits of DLT and its maturing regulation, it is highly unlikely that any business is ready to ditch fiat’s rails entirely. Coexistence will be the norm, and with that the need for solutions that let consumers and businesses use ‘old’ and ‘new’ cross-border payment methods in tandem or interchangeably.

FAQs

How big is the cross-border B2B payments market in 2023?

The value of the overall global cross-border payments market will grow from $190 trillion to $290 trillion by 2030, according to FXC Intelligence. Of that, B2B payments will grow from $39.3 trillion to $56.1 trillion in the next seven years.

What are some common reasons businesses and people need to move money internationally?

Common reasons businesses and people need to move money internationally include e-commerce, remittances, international trade, travel, business payouts, trading platforms, and domiciling company funds.

What are the benefits of cross-border payments?

Cross-border payments offer a range of benefits to businesses, such as the ability to open new markets, increased efficiency, cost savings, and improved cash flow.

What is risk in cross border payments?

Risk in cross border payment methods is defined in a number of ways. Businesses are at risk of payments failing, long settlement times, costly processing fees, poor payment experiences and complex regulatory obligations. These risks can impact cash flow and market competitiveness.

What are the leading payment methods for cross-border transactions?

Popular payment methods for cross-border transactions include credit and debit cards, wire transfers, global ACH, fintech networks, blockchain and cryptocurrencies.

What is Swift?

Swift (the Society for Worldwide Interbank Financial Telecommunications) is the primary network for moving money internationally, with 11,000 member institutions worldwide and facilitating $150 trillion in transactions per year.

How is blockchain used in cross-border payments?

Blockchains are used in cross-border payments in a number of ways. Cross-border payments can be made directly on-chain if the transaction is being initiated and settled in the same cryptocurrency. Blockchains can also be used as an intermediary tool to process cross-border fiat payments. The payer’s fiat currency is converted for a cryptocurrency, sent across the relevant blockchain, and converted to the payee’s preferred fiat currency for settlement. Stablecoins are often used for this because they are less volatile.

What are the benefits of using blockchain for cross-border payments?

The benefits of using blockchain for cross-border payments include faster settlement, lower costs, fraud prevention, security, easy deployment, and stability.

What are the advantages of using fintech networks for cross-border payments?

The benefits of using fintech networks for cross-border payments include automatic rerouting of payments to identify the fastest and most effective settlement path; real-time information about the progress of the payment; ease of integration with other services, such as FX; management of compliance obligations; and enhanced customer support.

What should I consider when deciding on a partner to support my business with cross-border payments?

When selecting a payment provider to support your business with cross-border payments, you should consider their coverage, breadth of capabilities, ease of deployment, processing times and fees, technical support, and compliance.

Summary

Businesses willing to embrace the opportunities of more efficient cross-border payments have lots to gain, including lower operating costs, improved cash flow, and deeper market penetration. But cross-border payments are also becoming more complex. Businesses must navigate a growing number of payment methods and providers, dislocated regulatory landscapes and markets that have customers with different habits and expectations. Neither do any of these factors stay still for long.

Partnership is key. The technical aspects of moving currencies across borders, or between fiat and blockchain rails, can be easily outsourced. That said, businesses must have a clear set of criteria and priorities when selecting partners. The bigger opportunity comes when partners get involved early and can influence the overall payment strategy, when all options are still in play.

For most businesses, trusted legacy systems and deep-rooted behaviours will mean a period of coexistence between traditional banking payment rails and new alternatives. But it will not be long before the evidential advantages of emerging cross-border payment technologies will make their widespread adoption inevitable. Of those battling for dominance, DLT and blockchain payments have most to offer, especially where stablecoin currencies are used. Ironically, the most significant of these benefits is that payments using them have no borders to cross.

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

{kind=link}

Never miss an insight.