Using bitcoin to transfer money internationally: a 2023 guide for businesses

Introduction

Bitcoin, and other cryptocurrencies such as stablecoins, can help businesses send and receive international payments more easily. By using new blockchain technology, businesses can avoid some of the frustrations associated with traditional cross-border payment systems, such as slow processing times, dislocated technologies, opaque costs, and poor access to emerging markets.

In this latest article in our series on international business payments, we will explain how bitcoin, stablecoins and cryptocurrencies more generally are changing B2B cross-border payments and settlement, how they work, and how to enable them as part of your payments strategy.

Understanding bitcoin and stablecoins: revolutionising B2B international payments

The global cryptocurrency market cap is $1.08 trillion. That would put it comfortably in the top 20 economies in the world. Of that market, bitcoin (the oldest operational cryptocurrency, having launched in January 2009) is by far the largest, with a market cap of almost $512bn, accounting for 47% of the entire market. Stablecoins, which are a category of cryptocurrencies (of which there are almost 100 varieties in circulation) is collectively worth almost $124bn, about 12% of the market.

Bitcoin and stablecoins are both digital currencies that can be exchanged using blockchains. A blockchain is a ledger that both enables transactions of cryptocurrencies directly between users, and records those transactions. Bitcoin’s blockchain is decentralised, meaning no one organisation or person ‘owns’ the bitcoin network, but instead its operation and oversight is shared by computers (known as ‘nodes’) that are distributed around the world.

Stablecoins use a variety of blockchain technologies, with differing levels of decentralisation. While blockchains vary in their governance and operating rules, when it comes to using them for business to business payments, they tend to offer faster settlement times, lower costs, reduced operational complexity, and improved access to emerging markets, compared with traditional banking and card networks.

That said, it is worth noting that many businesses are using bitcoin and stablecoins in conjunction with fiat currency transactions as means to move funds between markets.

Bitcoin’s role as a disruptor in international money transfers

Hundreds of thousands of bitcoin transactions take place every day. Many companies choose to accept payments in bitcoin from customers around the world, and consumers can easily make global peer to peer payments with bitcoin.

But bitcoin isn’t typically used by businesses to facilitate international payments and money transfers. Though bitcoin has many advantages over traditional fiat payments (which we discuss in this article), its price volatility creates too much risk and uncertainty for businesses.

The underlying blockchain technology that cryptocurrencies run on however, has emerged as a viable alternative to traditional cross-border payment methods for a variety of reasons: blockchains operate 24/7, the cost of transacting is negligible, settlement is full and final, access is available to anyone with an internet connection, and the technology has been proven to work securely.

One report from 2022 says that more than 37% of businesses are currently using blockchain and cryptocurrencies like stablecoins for cross-border transactions. While Juniper Research estimates that the total value of blockchain-enabled B2B cross-border payments will exceed $4.4 trillion by 2024; up from $171 billion in 2019. We are also seeing established payment providers explore blockchain. Visa B2B Connect, launched in 2019, is a blockchain-enabled payment solution to facilitate global transactions between banks, without the need for a card; while Mastercard Send also leverages a private blockchain to enable near real-time cross-border payment transfers between billions of card, bank and digital accounts globally.

Of the different types cryptocurrencies available, stablecoins are the most suitable for paying and transferring money internationally because they provide price stability.

We are seeing this firsthand at BVNK. Of the total payments collected on behalf of our business customers through BVNK’s Global Settlement Network between 2022-2023, two thirds were stablecoins, while only 6% were bitcoin payments. Sometimes, our customers use stablecoins as an intermediary bridge between two fiat currencies to accelerate settlement, although 15% of our collected payments were also settled in stablecoins. We will explore the benefits of stablecoins versus bitcoin in more detail later in this guide.

Step-by-step guide: how to use bitcoin for international payments

With a bitcoin payment the payer and payee are operating on the same rails, with the same currency, data formats and protocols. This allows them to transact directly, regardless of what country they are in. Here's an example of how it works:

- Payment request: The payee provides the payer with a public bitcoin address.

- Initiation: The payer opens their cryptocurrency wallet and sends bitcoin funds to the payee’s address, also paying the blockchain’s processing fee.

- Broadcast: The transaction request is broadcast to users on the bitcoin blockchain and checked by nodes to ensure the payer has enough bitcoins to make the payment.

- Block submission: The transaction is submitted to a block, awaiting miners to validate it.

- Approval: A transaction is typically approved after a validated block has been certified by enough nodes, which can take a few minutes. If you're using a fintech partner to process bitcoin payments for you, your fintech partners may be able to guarantee the confirmation for you, giving you instant approval.

- Settlement: The transaction is completed and recorded on the blockchain – and the payer and payee wallet balances, updated.

In reality, the main reason that businesses would use bitcoin is for international consumer payments, in countries where it is popular, where the domestic fiat currency is subject to high inflation, and with high levels of financial exclusion and poor banking infrastructure.

Many companies who choose to accept bitcoin from global customers also opt to work with fintech partners who exchange the bitcoin on their behalf, settling them in their preferred fiat currency, meaning they don’t need to hold crypto assets on their balance sheet.

Bitcoin is less commonly used for facilitating B2B international payments because of the issue we have already discussed around its price volatility. Stablecoins are more suitable and in wider use here.

As we will read in the next section, stablecoins are a better alternative to bitcoins for this as they hold their value, and so mitigate the risk of currency slippage. BVNK’s own cross-border payment solution — Global Settlement Network — uses stablecoins to help businesses process fiat payments from anywhere, to anywhere in the world, and to seamlessly trade between currencies.

The pros and cons of using bitcoin for B2B international payments

There are a number of pros and cons of using bitcoin for B2B international payments. Let’s first take a look at the benefits.

The unique technology of blockchains, and their separation from traditional banking and payment networks, provides businesses with a number of benefits when making cross-border transactions.

Fast, always-on settlement

Settling money internationally using banking systems like Swift can take several days, particularly when moving funds in and out of emerging markets. Finance teams have to resort to pre-funding or suffer cash flow pressures. Settlement on blockchains using digital currencies can be near instantaneous and carried out 24/7 (though you’ll need to add time if you want to convert the cryptocurrency for fiat), eradicating the cash flow gap between the costs of selling and the revenues from sales.

Cost efficiency

Bitcoin payments allow for straight-through processing between payer and payee (though in reality third-parties, such as wallet providers, fintech platforms and currency exchanges are commonly used) In comparison, traditional cross-border payment systems can require multiple intermediary banks (also known as ‘corresponding’ banks) to support the path of a payment, which adds settlement time and costs. One study found that blockchain-enabled cross-border payments could save businesses $10 billion by 2030.

Reliability

Bitcoin has been proven as a method for securely making international transactions. The volume being transferred daily on the bitcoin blockchain shows it is a reliable and trusted medium of exchange (though it is worth noting that this chart includes consumers payments,) that is highly resilient against cyber attacks.

Adoption ease

An entire bitcoin-enabled payments operation can be outsourced to a third-party, giving a business all the benefits with none of the risk or compliance obligations of holding them as assets on its balance sheet.

Transparency and traceability

While the bitcoin blockchain doesn't directly reveal payer and payee information, it does allow for the traceability of transactions through public addresses and the publication of immutable records. This provides a high degree of visibility on the status of a payment, and aids payment reconciliation, financial record-keeping and analysis. A distributed public ledger also provides a powerful tool to track the provenance of funds, and detect and prevent illicit payments activity.

Decentralised

With bitcoin, no single organisation is in charge. Bitcoin is managed by a protocol that was embedded into its network from the start and is maintained through a consensus mechanism. This determines when new bitcoins are issued, who to, and how transactions are verified. The collective incentive of users to maintain the integrity and security of the system has made bitcoin virtually impossible to subvert for individual gain, while the underlying technology has proven to be resilient against cyber attacks. Compare that with traditional payments, which run across centrally controlled card and banking networks. The owners of these networks can decide who gets access, and how much to charge users. Those without permission get locked out. Bitcoin is permissible by default, meaning any business with an internet connection can participate.

Fast innovation

The bitcoin blockchain is an open-source technology, meaning anyone can be involved in its future development. There are plenty of examples of this. The Lightning Network is a layer-two scaling solution built on top of the bitcoin blockchain that enables faster and cheaper ‘off-chain’ transactions. This makes bitcoin more suitable as a payment method, especially for small value transactions.

Now let’s look at some of the main challenges of using bitcoin for making B2B international payments.

Intermediaries

As with fiat currency payments, businesses typically use intermediaries, such as cryptocurrency exchanges and payment processors to send, receive and convert bitcoin payments. These intermediaries charge fees and require additional administration, such as Know Your Customer (KYC) and Anti-Money Laundering (AML) checks.

Price volatility

A major criticism of bitcoin is its price volatility. In the last 12 months alone, bitcoin’s price has been as high as $31,446, and as low as $15,814. What’s more, the price can swing very dramatically. For businesses, this unpredictability makes it difficult to price products and services accurately, determine the optimum time to convert bitcoin into fiat or another cryptocurrency, or hold bitcoin on the balance sheet.

Technical knowledge

Bitcoin payments require users to have a certain level of technical expertise and familiarity with digital wallets and cryptographic keys. The complexity of the user experience, especially securing private keys and protecting digital wallets, can be a barrier to business adoption, though much of this complexity can be offloaded to a trusted payments partner

Regulatory compliance

As a digital asset which can be exchanged across borders, bitcoin raises regulatory and compliance challenges for businesses. Governments and financial institutions are still developing frameworks to regulate and monitor bitcoin payments, including AML and KYC requirements. The global picture is mixed and continually evolving. For example, a very recent court ruling in Shanghai may reverse the outright ban on bitcoin in China and pave the way for it to become legal tender. Businesses may find it hard to navigate this uncertainty, especially those that operate in multiple markets.

Energy consumption

The bitcoin blockchain network leverages a proof-of-work consensus mechanism, which consumes substantial amounts of energy. The environmental impact of energy-intensive blockchain operations can be a concern for businesses that are obligated to meet climate impact benchmarks. That said, bitcoin mining is energy-agnostic, and can be situated in locations with access to relatively cheap and renewable sources.

Stablecoins vs bitcoin for B2B international payments

Stablecoins have become established as a superior alternative to bitcoin for B2B international payments, because they provide far greater price stability. Payments worth billions of dollars are made every day using stablecoins, with settlements reaching approximately $8 trillion in 2022, surpassing volumes of major card networks like Mastercard and American Express. By the end of 2023, it’s expected that on-chain stablecoin volumes will exceed those of Visa, the world’s largest card network.

Just like bitcoin, stablecoins run on blockchains that operate 24/7, and so can be traded and exchanged around the clock with almost immediate settlement. In contrast, most stablecoins operate across multiple blockchains. This interoperability promotes liquidity and use across decentralised finance (DeFi) platforms and ecosystems. It also means stablecoins can be processed more efficiently, especially during times of high network congestion, by utilising blockchain networks with faster transaction confirmation times and higher throughput.

At BVNK, we see stablecoins as the most effective cryptocurrency for enabling cross-border payments and settlements. Their price stability, deep liquidity and multi-blockchain trading rails overcomes many of the frustrations that businesses have with traditional cross-border payment methods.

Stablecoins and forex risk

One of the most significant challenges of making B2B international payments is forex risk. Any business with foreign buyers or suppliers needs to convert currencies at low cost, at speed, and when prices are favourable. Conversely, when any of those factors are not managed effectively, there are significant cost and revenue implications. This is what we mean by forex risk.

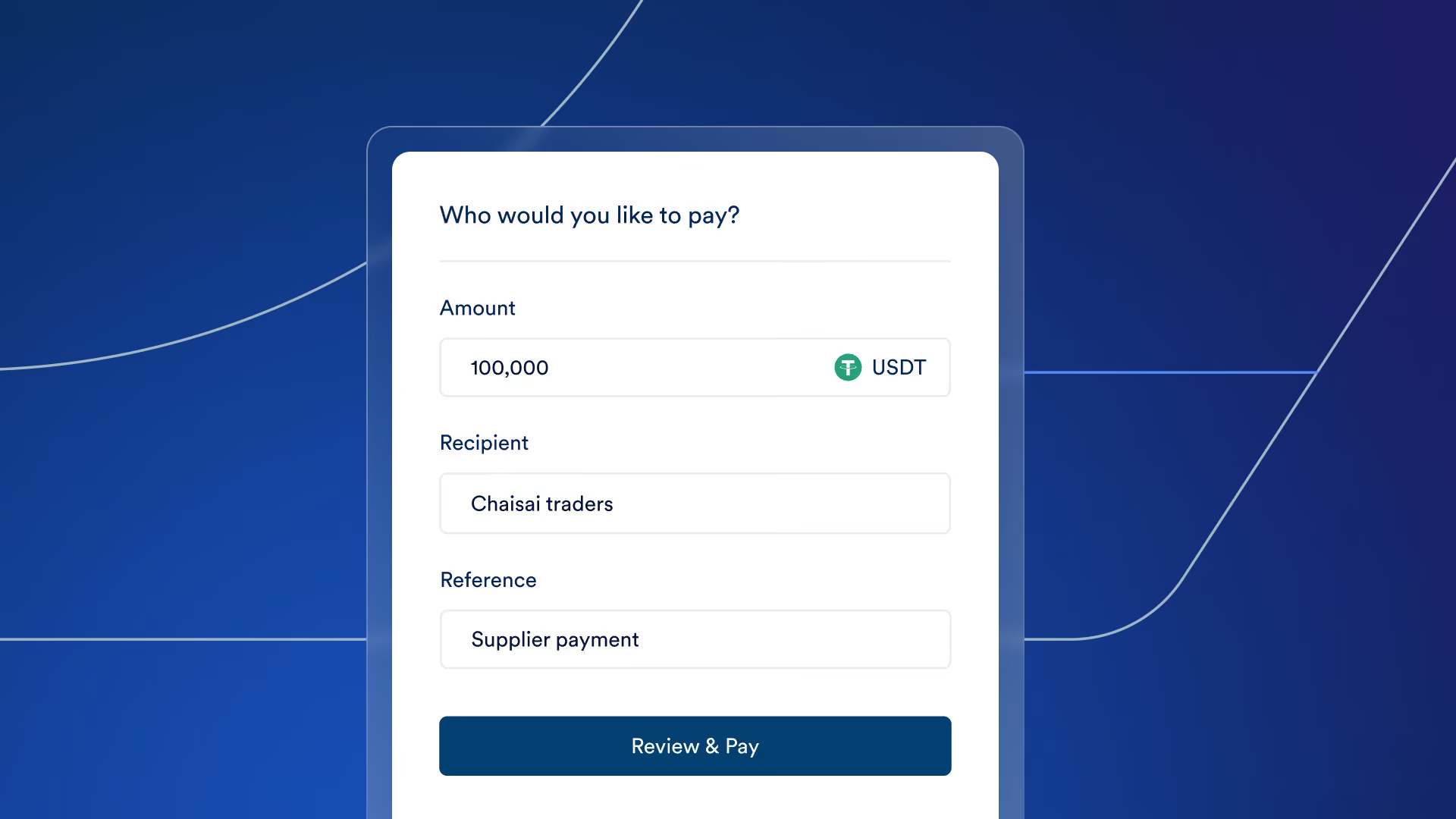

Stablecoins are an effective way for businesses to mitigate forex risk in payments, because they operate independently of traditional international payment rails and have been proven to hold their value relative to a fiat currency, typically the US dollar. Businesses can either trade directly in a stablecoin, or use a stablecoin as an intermediary currency to accelerate a forex transaction. Below is an example of how BVNK facilitates cross-border payments using stablecoins. Read our guide: How to manage foreign exchange risk in 2023.

Stablecoins do have their own risks. Over the past few years, some stablecoins have broken their price peg, though in most cases stability was reinstated promptly. There is also heightened counterparty risk. Unlike the decentralised nature of bitcoin, most of the leading stablecoins are issued and administered by a central company. Mismanagement of reserve funds, operational vulnerabilities and cyber attacks are more likely as a result. Businesses do need to be aware of these risks, and understand the benefits from offloading management to a third-party provider, such as BVNK.

Read our complete guide to using stablecoins for business payments.

How to send cryptocurrencies to a business bank account

To send cryptocurrencies to a business bank account, you first need to exchange it for fiat currency. Bitcoins, stablecoins and other cryptocurrencies can be easily exchanged for fiat currencies using a payments partner, and then deposited to a corporate business bank account.

If a business is using a cryptocurrency like stablecoins as a forex bridge to enable a fiat-to-fiat international transaction, then the exchange and final settlement happens behind the scenes, and is usually enabled by a third party provider.

Alternatively, a business can hold reserves of any cryptocurrency in dedicated wallets, and then exchange for fiat and deposit to a business bank account at a time of their choosing. Let’s now look at how that process happens.

Registration: A business will need to have an account with a cryptocurrency exchange, or a third-party payments provider that can provide access. Both options will require the business to complete compliance, such as KYC and AML checks, and typically nominate a fiat business bank account for deposits and withdrawals.

Deposit: Deposit the cryptocurrency you want to convert from your own crypto wallet into your wallet with the payment or exchange provider.

Sell: Place a sell order on the exchange. For an immediate sale, businesses will use the market price offered by the exchange. For large trades, it may be more effective for a business to use the OTC service of a partner.

Execute: Once a buyer is found, the trade will execute, and your cryptocurrency will be sold for the equivalent amount of fiat currency, minus any fees. The funds will be held in a fiat account on the exchange, or on the partner’s platform.

Withdraw: Instruct the exchange or partner to send fiat funds to your nominated business bank account. A bank network, such as Swift, SEPA or Faster Payments, will be used to process the settlement. Settlement times can vary, from hours to days, depending on the bank network used.

How a fintech partner can help

Many businesses choose to work with fintech partners to help them convert cryptocurrencies into fiat and deposit into their business bank account.

Let’s look at how this works, using BVNK as an example fintech partner.

- Login to your BVNK account and fund your crypto wallet. (With BVNK, each cryptocurrency and fiat currency is held in separate virtual accounts.

- Select the amount to pay out, and the fiat currency you want to settle in.

- BVNK provides a quote for the exchange, which is locked in once accepted.

- BVNK exchanges the cryptocurrency for the fiat currency of your choice.

- BVNK updates the balance of your cryptocurrency and fiat wallets accordingly and the transaction is complete.

- You can then make a fiat deposit to your business bank account from BVNK's platform. Learn more here

The future of B2B international money transfers: cryptocurrencies vs. traditional methods

Cryptocurrencies are not the only innovation currently shaping the future of B2B international money transfers. Banks, card networks and fintechs have also been hard at work to improve traditional methods of cross-border business payments and settlements.

A key trend is collaboration, not just between companies, but also across different payment verticals. This climate of collaboration points to a period of coexistence, as businesses get easier access to new solutions while retaining tried and trusted methods. Let’s take a look at some of these examples of innovations and collaborations.

Swift innovations

Swift gpi (‘Global Payments Innovation’) was launched in 2017, unifying previously dislocated domestic real-time payment networks. It uses a unique end-to-end transaction reference (UETR) to pinpoint the status of payments in real-time, and redirect them to faster paths. It also offers a pre-validation feature, which reduces the likelihood of transaction failure. Swift gpi already enables $300 billion of daily transactions, 50% of which are completed within 30 minutes, and 96% in under 24 hours. In 2021, Swift Go was launched on this new payment rail, and is targeted at SMBs that make low-value (less than 10,000 USD, GBP or EUR) cross-border payments. More recently, a collaboration with Visa illustrates Swift’s appetite to improve and grow through partnerships.

New international banking networks

India and Singapore have recently linked their digital payments systems, UPI and PayNow, to enable instant and low-cost fund transfers, with customers from eight banks able to benefit. Pix, Brazil’s domestic instant payments system, is exploring integrations with banking networks in the US, Colombia and Canada.

Multi-bank APIs

There are more than 90+ live bank APIs available globally, which businesses can use to make cross-border payments and money transfers. Until recently, bank APIs have not been a popular method because they have been difficult to enable. Most businesses would need to connect at least four bank APIs (balances, transactions, payment initiation and payment status) across each of their banks; and multinational corporations can have many banking partners. Consequently, they have suffered from a lack of scale; in other words, businesses can only make and receive payments with other businesses that have bank APIs enabled.

The multi-bank API aggregator overcomes this challenge by integrating multiple bank APIs into a single interface and unified API. Using APIs and open banking protocols, businesses can benefit from faster payment times and easier integrations with other financial and treasury software systems. Some leading bank API aggregators include Plaid andTrueLayer.

Fintechs

Fintechs layer services on top of banking networks, usually leveraging their APIs, to solve some of the traditional challenges of moving money internationally. Examples of these services include pre-funding to simulate 'instant' payments, automatic rerouting of payments to identify the fastest and most effective settlement path, real-time information about the progress of the payment, ease of integration with other services, such as FX, management of compliance obligations, and enhanced customer support.

A fintech provider allows businesses to offload much of the work involved in processing cross-border payments, freeing up resources that can be redeployed to core activities. Some of the leading B2B cross-border payments fintechs are Airwallex, Nium, and Wise.

Blockchain partnerships

Stripe, one of the world’s largest fintechs, now offers merchants the ability to make payouts in cryptocurrency through the stablecoin USDC, which is issued by crypto firm Circle. Visa is now allowing its partners to send or receive USDC settlement payments via the Solana blockchain, and says 15,000 financial institutions are currently using the service. Meanwhile, American Express has been working with Ripple since 2017 to process blockchain-enabled international B2B payments.

Central Bank Digital Currencies

CBDCs are another cryptocurrency alternative to enabling cross-border payments using blockchains. They are issued by central banks, and so provide greater regulatory protection. There are now over 100 CBDC projects around the world in various phases of development and testing, with fintechs such as Ripple providing the underlying blockchain technology, and coin issuance and management frameworks.

Wrapping up: Is bitcoin your best choice for B2B international payments?

While bitcoin has advantages such as speed, it has imitations including price volatility and an uncertain regulatory future. Increasingly, stablecoins are emerging as a more reliable option for businesses because they offer greater financial stability and predictability.

BVNK’s own cross-border payment solution — Global Settlement Network — uses stablecoins to help merchants move funds and settle between currencies quickly and reliably. One such customer is Noda, which uses BVNK’s Virtual Accounts and Global Settlement Network to convert around 4 million euros into stablecoins every month and pay out to their merchants. Read their story. It's just one example of how BVNK support hundreds of merchants to process billions in transactions every year using stablecoins.

While bitcoin and stablecoins offer advantages, it's crucial for businesses to adopt a pragmatic approach. A blend of traditional payment methods and cryptocurrencies can provide flexibility and risk mitigation.

Businesses should also work with experts in digital currencies to explore and enable the right solutions for them. As we read in the previous section, cross-border payments are enjoying a period of significant innovation, which can be hard to track. Appointing an international payments partner releases companies of this burden, while also offloading aspects of compliance, technical maintenance, and ongoing optimisations that deliver a more competitive cross-border payments operation.

FAQs

Is bitcoin suitable for B2B international transfers?

While many companies choose to accept payments in bitcoin from customers around the world, and consumers can easily make global peer to peer payments with bitcoin, bitcoin isn’t typically used by businesses to facilitate international payments and money transfers because of its price volatility. This unpredictability creates a number of issues for businesses engaging in international B2B trade, including the risk of currency slippage, difficulty pricing products and services, determining the optimum time to convert bitcoin into fiat or another cryptocurrency, or holding bitcoin on the balance sheet. Stablecoins share many of the benefits of bitcoin, while also being more resilient to price swings, and so are more suitable and in wider use.

How do stablecoins reduce forex risk in B2B international transfers?

In traditional forex transactions, exchange rates can fluctuate rapidly, which can lead to unexpected gains or losses for businesses engaged in cross-border trade. Stablecoins eliminate much of this exchange rate risk because their value remains closely tied to the pegged asset, and they are typically processed in near real-time, thus reducing the window during which exchange rates can move.

How much does it cost to make a B2B international transfer using stablecoins?

The cost of making a B2B international transfer using stablecoins can vary depending on a range of factors, not least the stablecoin being used. The cost will include a transaction fee (paid to the blockchain network), the conversion fee (when converting stablecoins into another currency), and the charges of the service provider that facilitates the stablecoin payment.

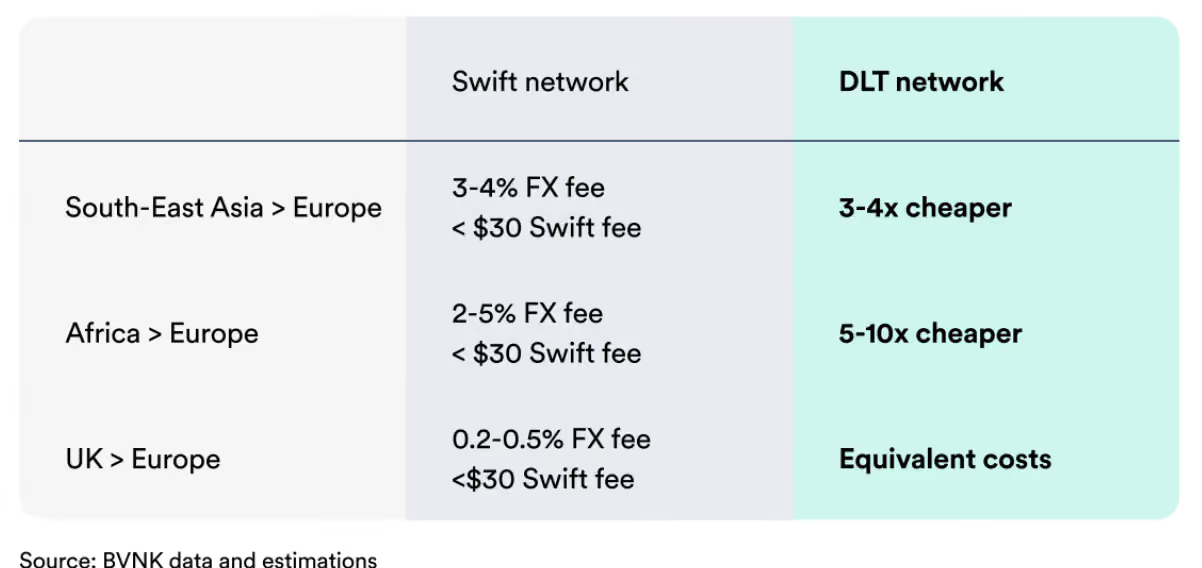

Blockchains are decentralised, cutting out intermediaries. Some studies suggest that businesses can save up to 80% on foreign exchange fees by trading stablecoins on-chain, instead of relying on the international banking system, Swift. If you’re converting in and out of fiat currencies, there are additional costs, but businesses can still achieve savings, depending on the provider and currencies (see table below). As with other payments, businesses with high volumes and low risk profiles are typically able to access better rates.

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

Never miss an insight.