Swift vs Ripple: 6 key areas of comparison for international business payments

Introduction

In a previous article we looked at some of the leading cross-border payment methods, which included Swift and Ripple. In this guide, we’re going to take a deeper look at Swift vs Ripple for making international business payments, with a comparison of speed, cost, compliance and more, to help you make an informed decision about how to move money across borders in the best way.

The need for efficient international payment solutions

While many traditional methods for making B2B cross-border payments are proven and trusted, businesses can be underserved by them. Dislocated banking networks, opaque costs and slow settlement times are just some of the challenges with established international payment methods.

These issues directly impact a company’s cash flow, supplier relationships, market competitiveness and profitability. In the last decade, the B2B international payments sector has witnessed significant innovation, all designed to fix these inefficiencies. Some of that innovation has come from incumbents, with Swift being the notable example. As we will note later in this article, Swift regularly releases new features and upgrades, while fintechs have emerged that are building upon Swift’s rails to create new services (eg Airwallex, Wise).

Other improvements have come from new wave of providers offering alternative methods for making cross-border transactions that operate independently of Swift and the traditional banking ecosystem – and instead use blockchain technology. Of this second group, some operate their own blockchain and/or native token (eg Ripple and XRP), while other providers are agnostic, giving you access to different tokens and blockchains (eg BVNK's Global Settlement Network).

A quick introduction to Swift and Ripple

Before we compare Swift and Ripple, let’s quickly profile each solution.

Swift

Swift is the Society for Worldwide Interbank Financial Telecommunications. It was founded in 1973, and became operational in 1977. In simple terms, it is a vast information messaging network that allows banks and other financial institutions around the world to send money to each other, by using a standardised code system. Today it is the dominant method for processing cross-border payments. It is used by more than 11,000 member institutions. Collectively they send an average of 44.8 million messages daily through the network. Read our dedicated article all about Swift.

Ripple

Ripple (owned by Ripple Labs) was founded in 2012. It is the majority holder of the XRP cryptocurrency that runs on the XRP Ledger public blockchain, and uses that to facilitate international payments. Since launch it has processed $30bn worth of volume and 20m transactions. It claims that its payments solution is faster, more transparent and more cost-effective than traditional financial services. It also provides cryptocurrency liquidity, digital asset management, and private ledger issuance and administration of stablecoins and CBDCs. All these products are enabled through RippleNet, a network of financial partners around the world. Unlike other cryptocurrencies that advocate complete independence from traditional finance, RippleNet is designed to work with banks and financial institutions as an alternative system for moving money globally.

Swift vs Ripple: 6 key comparison points for business payments

In this section we’ll compare Swift and Ripple against six key criteria. These are transaction speed, cost efficiency, the impact of intermediaries and correspondent banks, liquidity and currency support, regulatory compliance, and finally the scale of industry adoption and integration.

#1. Transaction speed

Transaction speed in international payments refers to the time it takes for a financial transaction to be processed and settled. Faster transaction speeds reduce the time it takes for funds to reach the recipient, improving cash flow.

Swift has had a reputation for slow transactions, with payments taking up to five days to process for some regions. The speed of a Swift transaction can be impacted by a variety of factors. These include the schedule of batch processing (Swift groups together transactions of a similar type and sends these as one), and the time of day (Swift transactions are typically processed during regular banking hours). Other factors affecting the speed of a Swift transaction include: a bank’s exchange rate policies and the specific currencies involved, the involvement of intermediary banks that handle the funds as they move from the sender to the recipient, the value and nature of the payment, and observance of regulatory obligations.

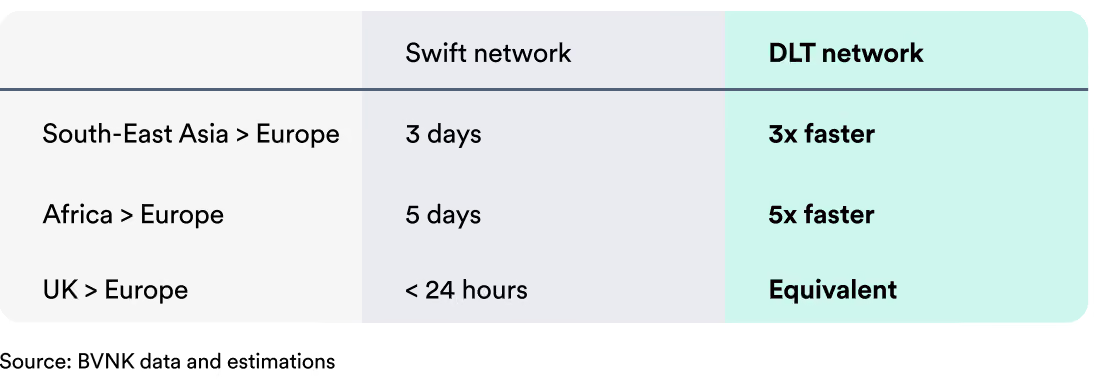

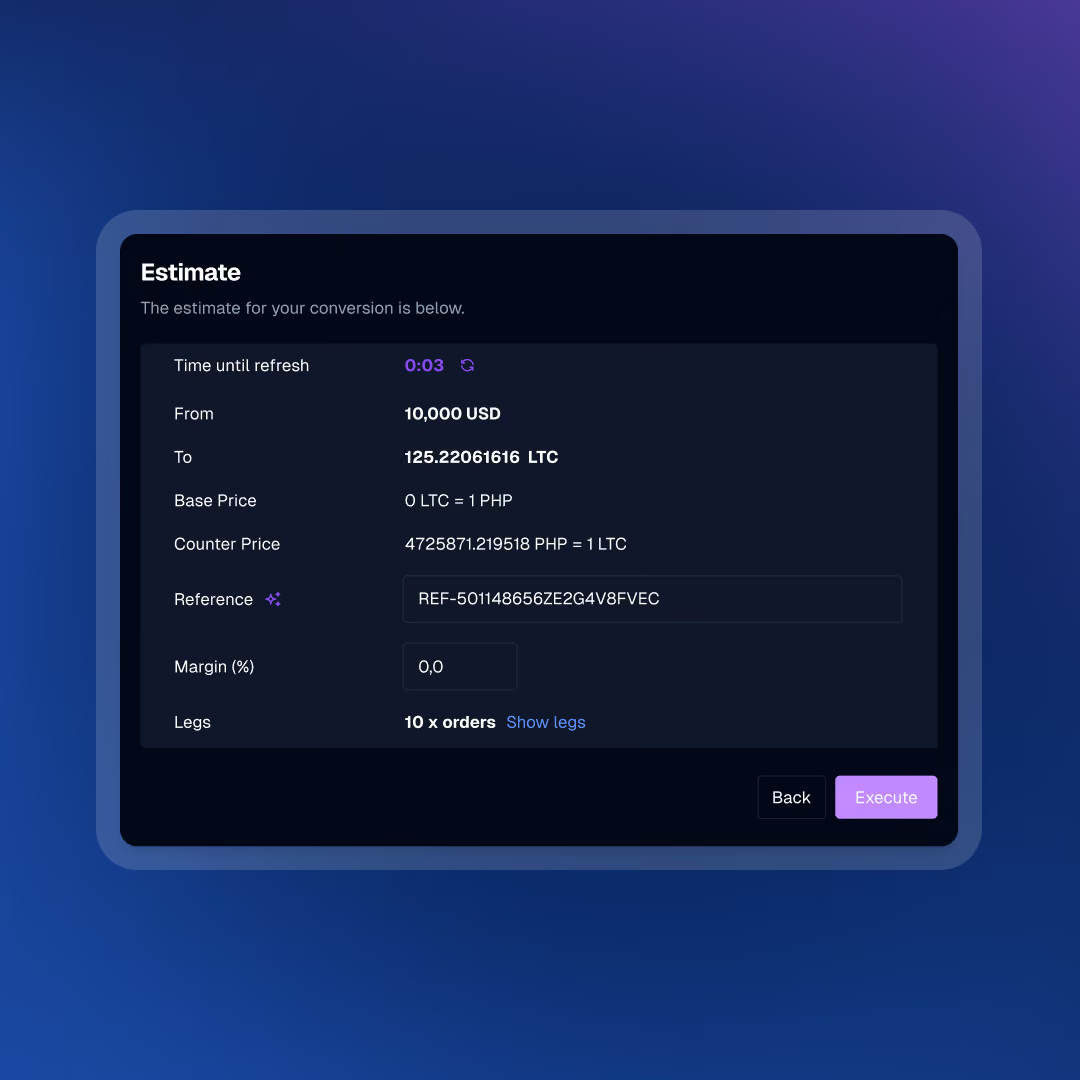

Here’s a simple comparison of settlement speed of a fiat to fiat transaction going via the Swift network, versus one that uses distributed ledger technology, eg a blockchain network.

In recent years Swift has delivered innovations that have improved transaction speed. Swift gpi (‘Global Payments Innovation’) was launched in 2017, unifying previously dislocated domestic real-time payment networks. It uses a unique end-to-end transaction reference (UETR) to pinpoint the status of payments in real-time, and redirect them to faster paths. It also offers a pre-validation feature, which reduces the likelihood of transaction failure. Swift gpi already enables $300 billion of daily transactions, 50% of which are completed within 30 minutes, and 96% in under 24 hours. In 2021, Swift Go was launched on this new payment rail, and is targeted at SMBs that make low-value (less than 10,000 USD, GBP or EUR) cross-border payments. Its fastest transaction had been recorded at just 21 seconds.

Ripple is known for its speed and efficiency in facilitating cross-border payments. It leverages blockchain technology, the XRP cryptocurrency, and the RippleNet network of institutional payment providers to expedite transactions. Ripple claims it can process international payments in seconds. However, the speed can vary based on several factors, such as network load, the availability and liquidity of fiat FX brokers, and compliance checks, notably ‘Know Your Customer’ (KYC) and Anti-Money Laundering (AML) requirements.

Ripple is only several providers using blockchain technology to improve international fiat payments. Our recent guide – Blockchain in cross-border payments: 2023 guide – is a great place to learn more about this exciting ecosystem. BVNK's next-generation payments platform for example, bridges the gap between traditional and digital finance to help merchants unlock the benefits of blockchain payments with minimal risk and technical setup.

#2. Cost efficiency

Cross-border payments involve several cost components, which can vary depending on the payment method, currency, and service provider. Here are the key cost components typically associated with cross-border payments:

Transaction fees

These are charges imposed by banks and payment service providers for processing the cross-border transaction. Both sending and recipient banks can apply fees. Transaction fees can be flat fees, a percentage of the transaction amount, or a combination of both.

Currency exchange fees

Also known as FX, currency exchange fees are levied when the payment involves multiple currencies that need converting. As well as the spread (the difference between the buying and selling prices of a currency) exchange services may apply a separate markup. FX fees are impacted by a currency's liquidity: banks, payment providers and FX brokers may need to hold a certain amount of funds in different currencies to facilitate cross-border payments for their clients. These liquidity costs include purchasing, holding and selling currencies.

Intermediary bank fees

Cross-border payments often involve multiple intermediary banks that handle the transfer of funds between the sender and receiver's banks. Each intermediary may charge a fee for their services.

Time value

The time it takes for cross-border payments to settle represents an opportunity cost, as funds are tied up and so cannot be used. The slower the settlement, the greater this cost.

Cost efficiency with Swift

There are several costs associated with using Swift, most notably fees for sending and receiving transaction messages through its network. These fees vary depending on the type of message and the volume of messages sent. Other fees are not in Swift’s control, such as FX conversion and charges that banks and other third parties charge for processing a payment. This creates an inconsistent and opaque fee structure.

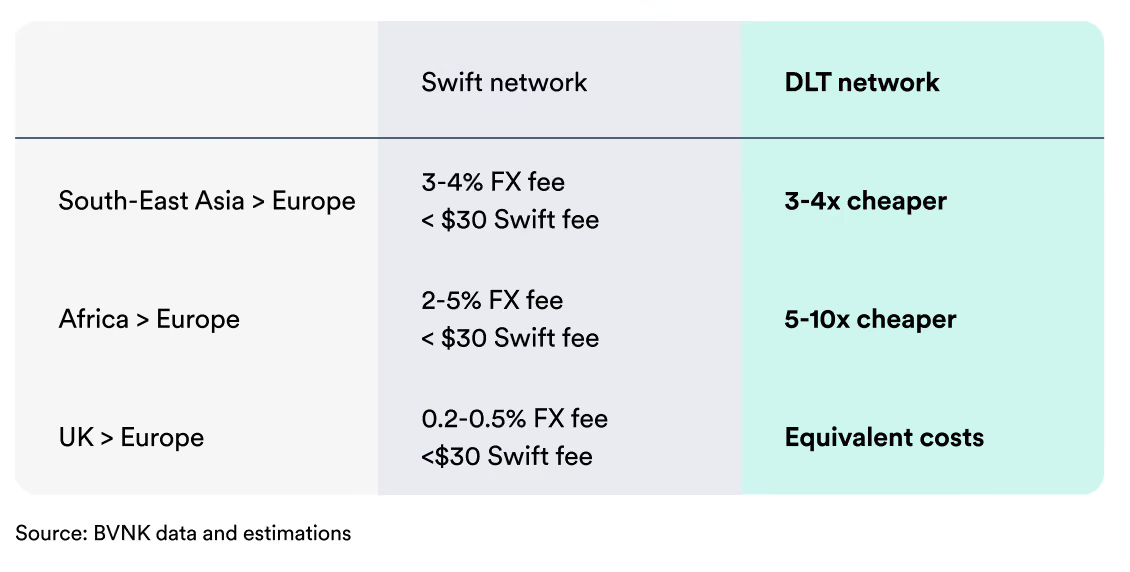

Here’s a simple comparison of transaction costs for a fiat to fiat transaction going via the Swift network, versus one that uses distributed ledger technology eg a blockchain network.

Cost efficiency with Ripple

Each transaction on the XRP ledger (the underlying blockchain that facilitates the payments) charges a minimum of 0.00001 XRP (10 drops - at time of publication, 1 XRP = $0.50.) Costs are added for more complex payments, such as those requiring multiple approvers or transferring to other users. Additionally, financial institutions commonly charge their customers to send money into and out of the XRP Ledger, for liquidity provision, to access the application, and for account maintenance.

#3. Intermediaries and correspondent banking: a closer look at Swift vs Ripple

Although intermediary and correspondent banks are vital for enabling international financial transactions, they can add costs to the process, including operational management and currency conversion. A complex transaction involving multiple intermediary and correspondent banks will also result in longer processing and settlement times, especially when banks are in different time zones.

Delays can also occur if there are communication issues, network disruptions, or if the message requires manual intervention at any point in the chain. There is also an increased risk of processing errors and payment failure due to differences in protocols and data standards between systems. As such, international payments involving intermediary and correspondent banks can be challenging to track, plan for and report on.

Intermediaries and correspondent banking with Swift

In traditional Swift transactions, intermediaries and correspondent banks play crucial roles in facilitating the movement of payment information and funds between the sender and recipient banks. When sending money internationally, the sender's bank may not have a direct relationship with the recipient's bank in another country. In such cases, intermediary banks act as a bridge.

They receive funds from the sender's bank and forward them to the next bank in the payment chain. While intermediary and correspondent banks provide a similar service, the former refers to institutions that support transactions in a single currency, while correspondent banks handle payments in multiple currencies.

Intermediaries and correspondent banking with Ripple

International payments with Ripple aim to eliminate the need for multiple intermediary and correspondent banks, enabling direct transfers between financial institutions. Ripple uses a combination of blockchain technology, and a global network of banks and payment providers (RippleNet), to allow financial institutions to transact directly with each other, wherever they are. Ripple uses XRP, a cryptocurrency, as a liquidity bridge. Financial institutions convert a fiat currency into XRP, send this across the XRP Ledger blockchain, and then convert it to the destination currency.

The elimination of third parties in that process delivers faster settlement times and reduces costs. Plus, transactions on the XRP Ledger are publicly reported in real-time, which reduces management costs of tracing and reconciling payments.

#4. Liquidity and currency support

International transactions often involve different currencies. Typically, businesses will rely on banks and payment systems to provide them with access to the currencies they need to make cross-border payments, rather than holding these on their balance sheets. This also eliminates some of the regulatory obligations involved with trading currencies. Payment systems offering currency liquidity and support enable more efficient flows of money.

Liquidity and currency support with Swift

Swift has developed the most extensive B2B global network of banks and financial providers. It is used by more than 11,000 institutions in 200 countries. This scale is one of Swift’s key strengths, because it enables connected banks to process transactions in almost any currency, and access deep pools of currency liquidity from other members. Also, Swift messages can include instructions related to currency conversion. For example, if a payment needs to be settled in a foreign currency, the message can specify the desired exchange rate. This directs FX transactions to the most appropriate provider.

Liquidity and currency support with Ripple

Ripple provides liquidity through its XRP cryptocurrency. When a payment needs to be made from one currency to another, XRP serves as an intermediary asset to facilitate the exchange. Financial institutions can access ‘on-demand liquidity’ of XRP in real-time from cryptocurrency exchanges or liquidity providers. This ensures they have sufficient XRP to meet their international payment flows, without the need to hold it (or various foreign currencies) in reserve, which can tie up capital.

#5. Regulatory compliance: considerations for Swift and Ripple

Regulatory frameworks governing cross-border payments vary by country and region, but there are some common principles and international standards. Every jurisdiction will have one or more government-related departments that sets and enforces the rules for cross-border payments. Their brief includes defining legal and regulated payment methods, issuing operating licences, setting capital controls, and preventing money laundering, terrorist financing, and other illicit activities. Compliance with these regulations is critical to avoiding legal action, financial penalties, and reputational damage.

Navigating regulatory compliance with Swift

Payments made with Swift carry a level of embedded compliance. Payment regulation requires specific details in payment messages, such as sender and recipient details, currency, amounts, the purpose of the payment and a reference number. These fields are standard elements of Swift’s messaging protocol. Swift also supports compliance with AML and KYC regulations by allowing institutions to verify the legitimacy of transactions and identify suspicious activities. Additionally, Swift transactions include message encryption, digital signatures, and are carried across secure transmission channels. Swift also provides additional products and services to support compliance with regulations.

Navigating regulatory compliance with Ripple

Regulation around the use of Ripple is complex. Blockchains and cryptocurrencies are largely unregulated mediums of payments, and the picture is evolving differently around the world. In addition, Ripple has faced specific regulatory challenges. In December 2020 the US Securities and Exchange Commission (SEC) filed a lawsuit against Ripple, alleging that XRP sales constituted unregistered securities offerings. In response, several cryptocurrency exchanges delisted or suspended XRP trading, causing a drop in liquidity. In July 2023 a judge found in favour of Ripple, a decision that the SEC has announced it will appeal. The case highlights the uncertainty of future regulations around Ripple (and other cryptocurrencies) regarding the classification of digital assets as securities or commodities. Ripple itself has advocated for more regulation to clarify this issue, and published a whitepaper on the subject in 2022.

#6. Industry adoption and integration

Payment systems benefit from critical mass. Scale establishes common standards and protocols that facilitate automation and lower unit operating costs. This enables financial institutions and payment service providers to connect and transact seamlessly, securely and cost-efficiently. The volume of transaction data can be leveraged to build powerful fraud-detection and predictive analysis tools. Scale also allows users to access new markets around the world. As more participants connect with a payment system, these economies of scale are strengthened.

Industry adoption and integration with Swift

Swift’s widespread adoption among banks and financial institutions globally is a result of its extensive network, standardised messaging, security credentials, and historical trust. Over 11,000 institutions across more than 200 countries benefit from these capabilities. It is overseen by the central banks of the G10 countries, the European Central Bank, and the National Bank of Belgium, which brings political legitimacy (and so stability). And it is ultimately controlled by approximately 2,400 member shareholders that represent financial institutions around the world and provide the necessary checks and balances. This member-ownership model also encourages innovation. Swift has proved resilient to technological changes; Swift gpi and Swift Go (as discussed earlier in this article) are examples of new services that maintain Swift’s competitiveness, while a collaboration with Visa illustrates Swift’s appetite to improve and grow through partnerships.

Industry adoption and integration with Ripple

Ripple’s network is a fraction of the size of Swift, but it has grown impressively. XRP is the fifth largest cryptocurrency by market cap ($26.8tr), and averages over $1tr in daily trades. Since its launch in 2012 it has processed $30bn worth of volume and 20m transactions. It has over 800 employees across 15 offices, and customers in over 50 countries. Though exact customer numbers are hard to find (it reported to have 300 in 2019), partners in its RippleNet network include iconic financial brands, such as American Express, Santander, PNC Bank, and most recently Wise. This reflects industry trust in Ripple’s technology and management.

How businesses use Swift and Ripple

We’ve collected some real-world case-studies, so you can read how organisations are actually using Swift and Ripple to enable cross-border payments.

- Swift and INA Group: By automating the communication process between INA’s ERP system, the Swift network and the respective banks, transactions are now more streamlined and secure.

- Swift and the National Bank of Australia: The National Australia Bank (NAB) replaced its existing Swift solution in 12 months, including simplifying and migrating around 2,000 routing rules.

- Swift and Suade Labs: Swift and Suade Labs teamed up to explore how to give regulators better and faster insights on market liquidity, while reducing the reporting burden on financial institutions.

- Ripple and Modulr: This partnership ensured Modulr customers can access reliable, real-time access international payments networks, driving economic value and benefits.

- Ripple and Tranglo: Ripple’s payments solution gives Tranglo access to +100 financial partners, allowing them to enter markets faster and at lower cost, while reducing the need to pre-fund destination accounts.

- Ripple and SBI Remit: SBI Remit is using RippleNet to power real-time remittance payments between Japan and Thailand, enabling 47,000 Thai nationals living in Japan to send money home faster.

Factors to consider when choosing between Swift and Ripple

Factors to consider when choosing between Swift and Riple for cross-border payments include integration with other financial systems, risk appetite, transaction volume and currency pairs. iSome financial institutions and businesses may enable both solutions for specific use cases and objectives.

Here is a reminder of some of the main pros and cons of each.

Pros of Swift

- Extensive network: Swift boasts a vast network of over 11,000 financial institutions across the globe. This extensive reach allows for comprehensive currency support and deep liquidity pools.

- Interoperability: Swift's standardised messaging protocols ensure that different banks can communicate and transact with each other effectively.

- Established industry standard: Swift has been a trusted and established system for decades, making it the default choice for many financial institutions. In turn, it benefits from the network effect.

- Regulatory alignment: Swift places a strong emphasis on adhering to international regulations and compliance standards; and the make-up of its shareholder and governing board means it often influences those rules too.

Cons of Swift

- Multiple intermediaries: Swift transactions often involve multiple intermediary and correspondent banks, leading to potential delays, added complexity, and increased costs.

- Lack of transparency: the use of multiple intermediaries can make it challenging to track the progress of a payment and understand the total costs associated with it.

Pros of Ripple

- Currency liquidity: Ripple's focus on using XRP as a bridge currency provides a streamlined solution for currency liquidity. It allows for efficient currency conversion, reducing the need for multiple currency accounts.

- Speed and efficiency: XRP transactions settle quickly, typically in a matter of seconds, which can minimise the time and exposure to currency volatility in cross-border payments.

- Cost savings: Ripple aims to reduce costs associated with cross-border payments by eliminating many intermediaries.

Cons of Ripple

- Market adoption: Ripple's network is still in the process of gaining widespread adoption. Limited participation ultimately reduces the extent of Ripple’s utility.

- Regulatory challenges: Ripple's use of XRP has faced regulatory challenges and media criticism in various jurisdictions. Regulatory uncertainty can stunt widespread adoption.

- Centralisation: Critics argue that Ripple's control over a significant portion of XRP tokens raises concerns about centralisation of power.

- Dependency on XRP: while other cross-boder payment providers are rail and token agnositc, Ripple's approach relies heavily on the adoption and stability of XRP as a bridge currency. Fluctuations in XRP's liquidity and value can impact its utility in cross-border transactions.

Conclusion: Beyond Swift vs Ripple

In this article we've explored the differences between Swift and Ripple. The key criteria we have looked at are transaction speeds, costs, the role of intermediary and correspondent banks, liquidity and currency support, regulatory alignment, and the scale of industry adoption. Each business should appraise these factors in the context of their own priorities and resources.

Of course, the market for cross-border payments is much larger than these two systems. BVNK regularly evaluates different cross-border payment methods on our blog, including other bank networks and cryptocurrency solutions.

An alternative to Swift and Ripple are stablecoins. We think stablecoins are likely to grow in popularity for B2B cross-border payments, because they provide deep liquidity, price stability, fast settlement, and are increasingly aligned with regulations. BVNK’s own cross-border payment solution — Global Settlement Network — uses stablecoins to help merchants move funds and settle between currencies quickly and reliably.

With more innovation in cross-border payments than ever before, it’s important for businesses to take time to research the best solutions for them.

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

.avif)

Never miss an insight.